Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

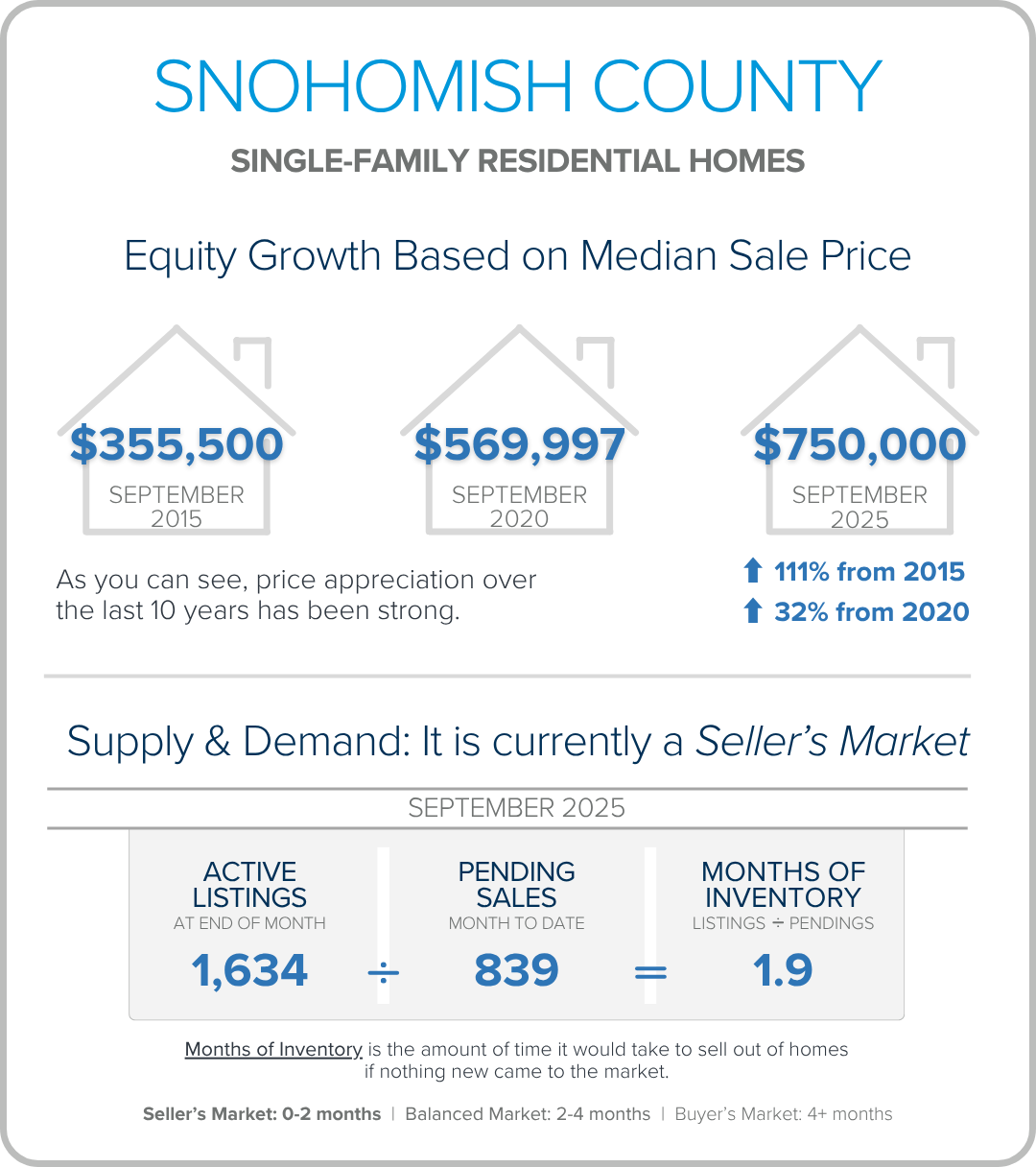

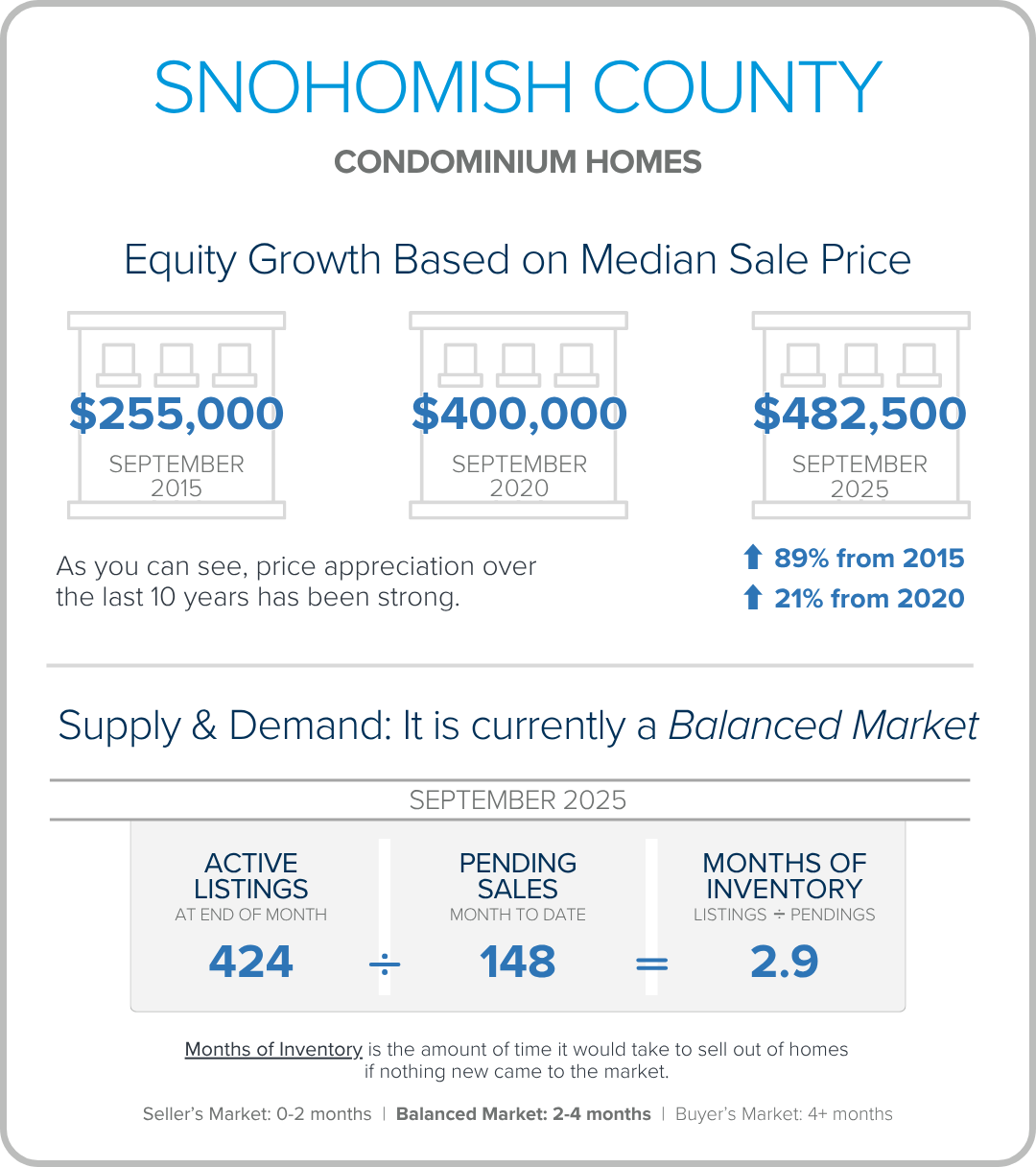

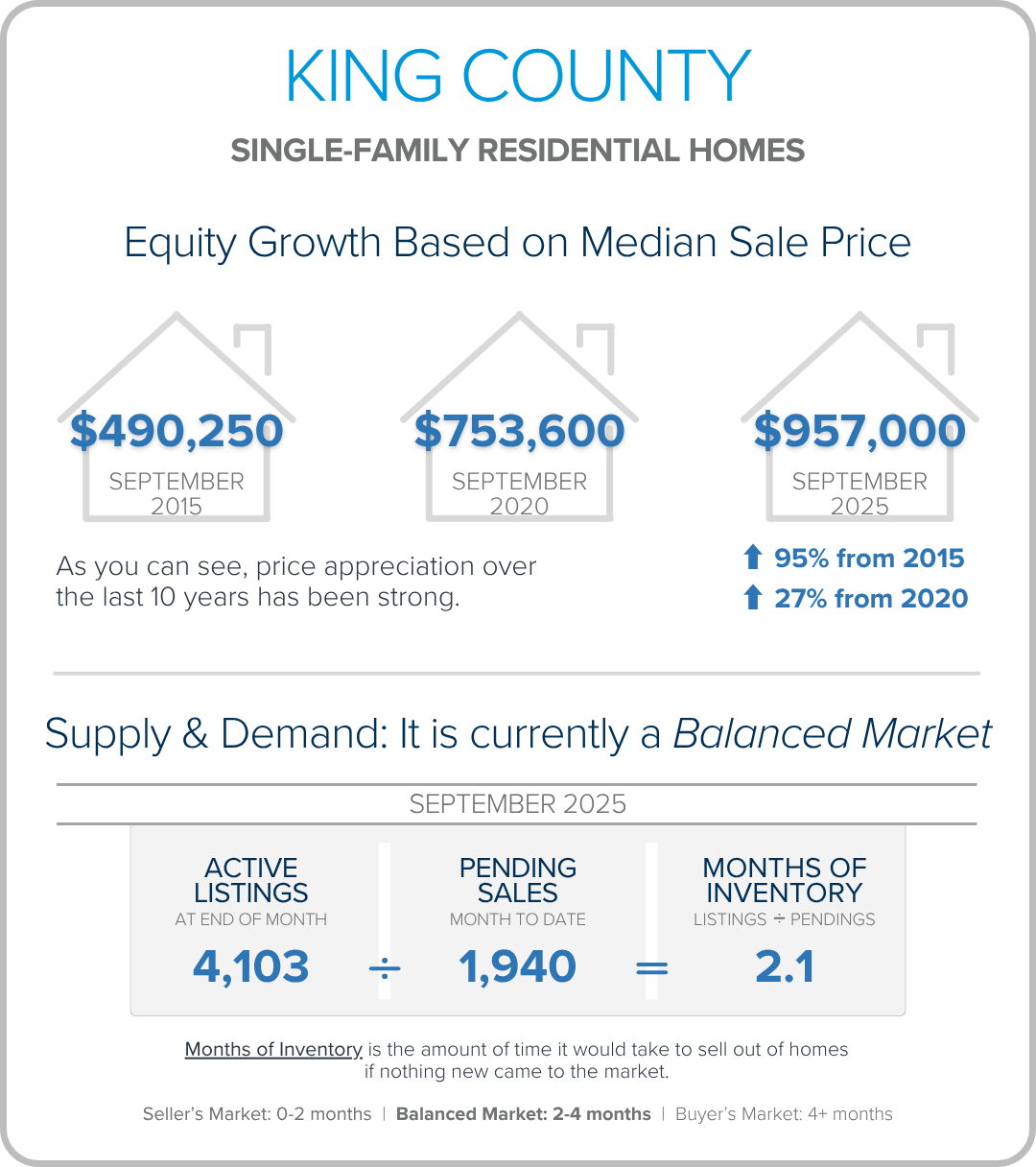

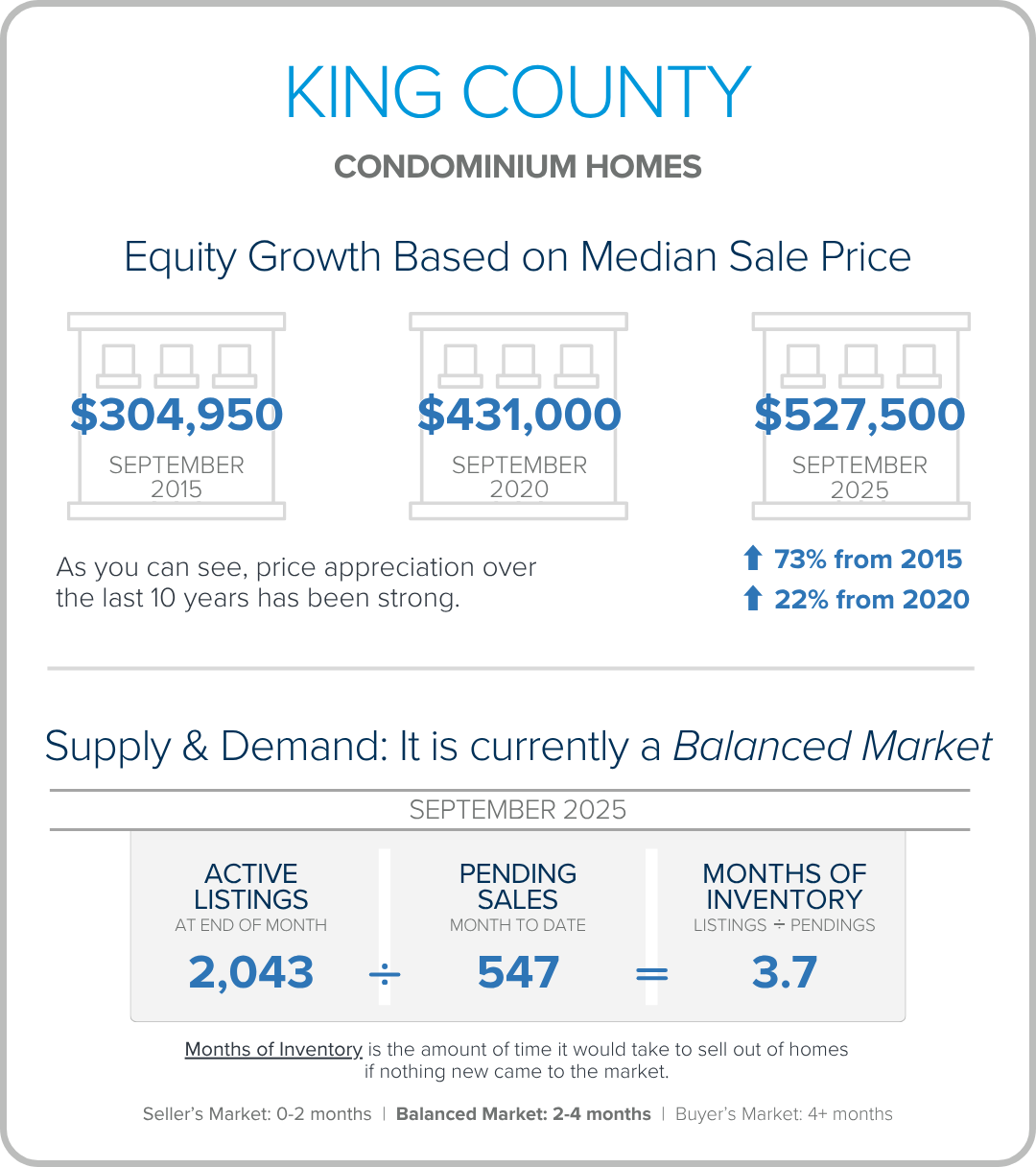

Let’s Celebrate: Equity & Inventory

As we round out 2025, we wanted to share some aspects of the current real estate market worth celebrating: equity and inventory! Below, you will see a 10-year equity study for Snohomish and King Counties, based on Single-Family Residential and Condos, along with a current assessment of inventory levels and their effects on the climate of the market. I felt it was important to bring you this information, whether you are a homeowner, renter, or if you are considering a move in the future. The market is finding balance, rates are gradually falling, and home values are maintaining.

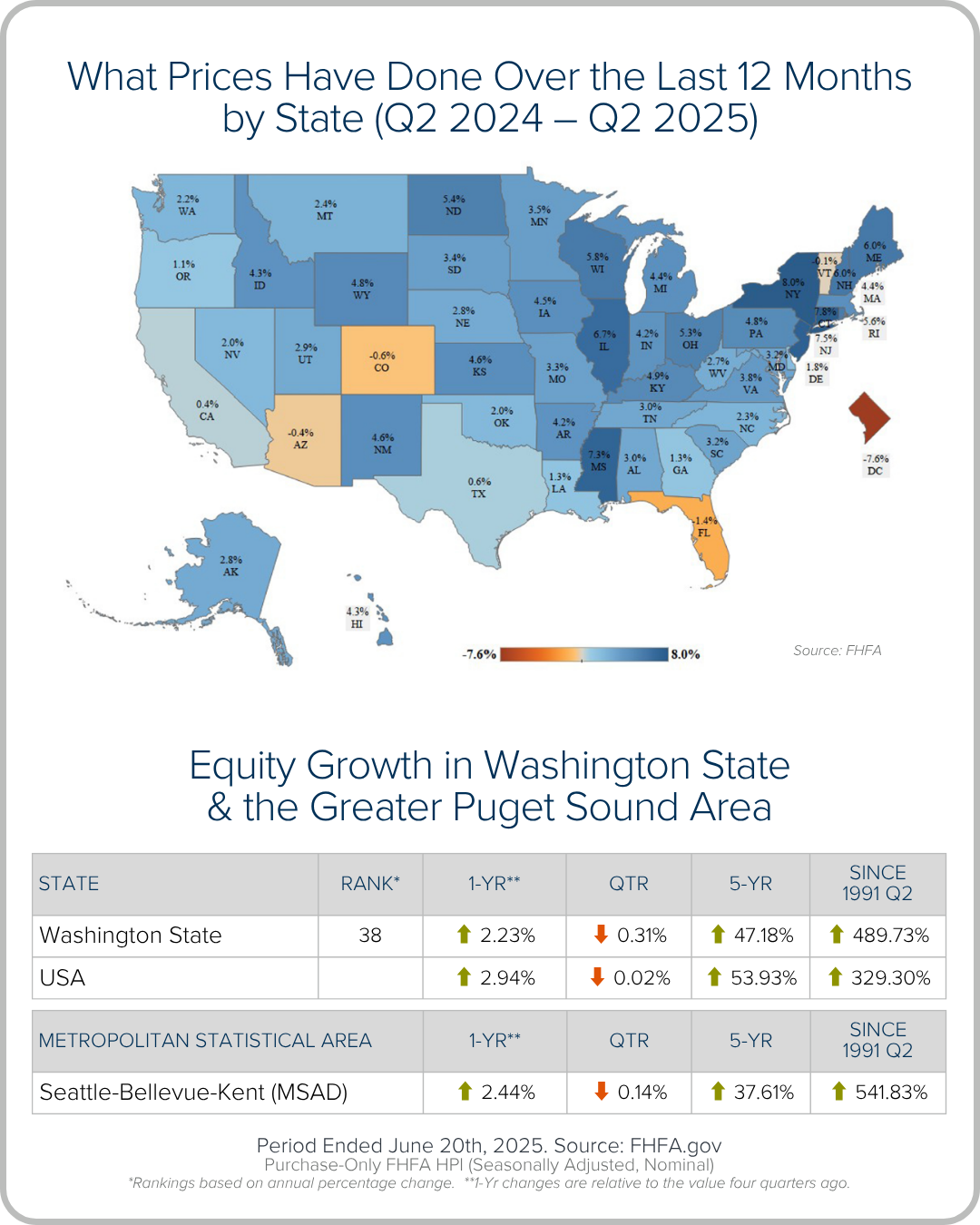

Home equity is incredibly strong in our region and is the backbone of household wealth for many. This nest egg provides financial security, can be a vehicle to create a move to a home that is a better fit for your lifestyle, or provide the funds to do a home remodel. The long-term hold investment in real estate continues to be a bright light economically.

Inventory levels have increased over the last two years and we are experiencing balance in the market which is providing opportunities for buyers to strike with less rush and frenzy. This has been especially beneficial for those who need to sell their homes in order to make a purchase. We’ve started to see an uptick in contingent sales and bridge loans to make a move smoother and more attainable. First-time homebuyers are also seizing the opportunity to lock in a lower interest rate and the affordability of stabilizing prices. Rates have decreased by nearly 1 point since May 2025.

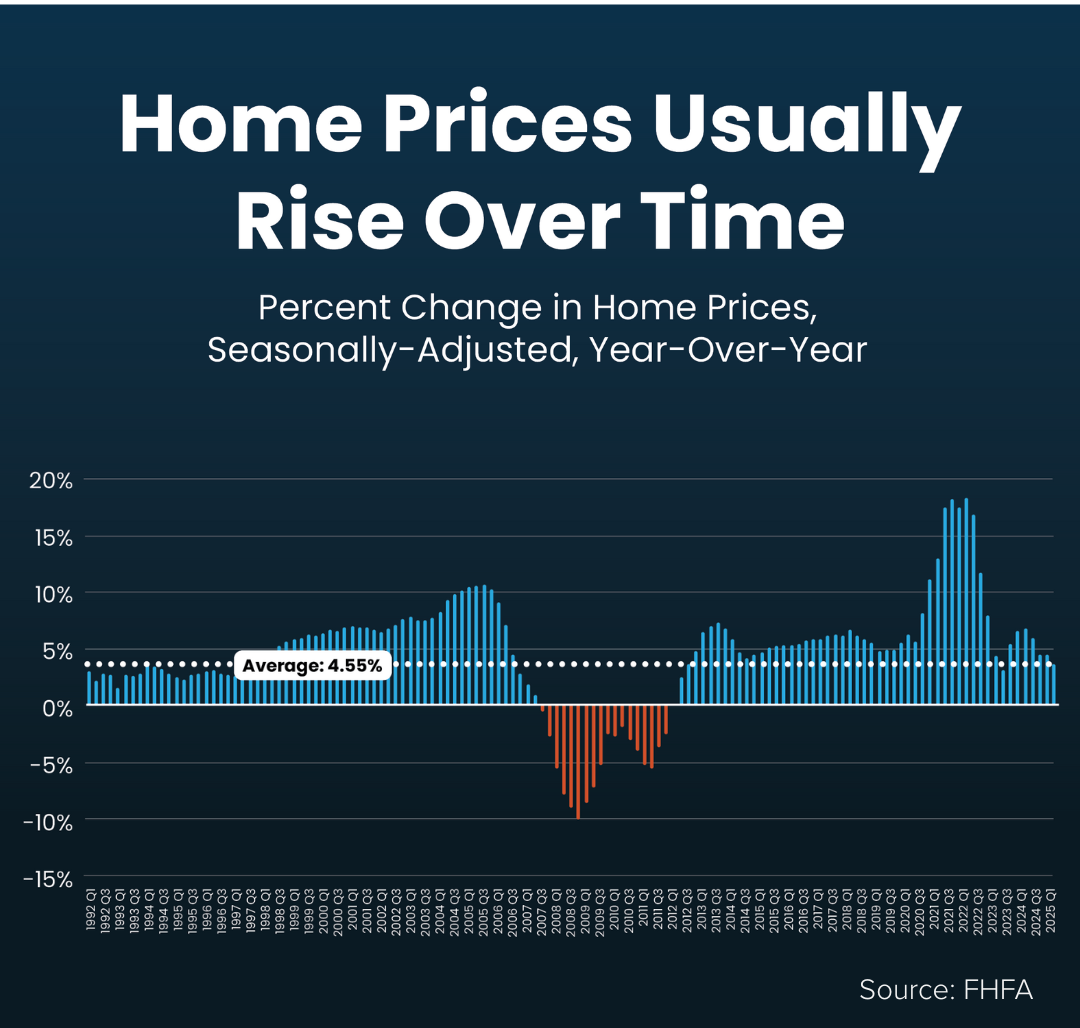

The image below from FHFA shows the long-term price growth (since 1991) in our state and metropolitan area. The figures are impressive at 480% in the state of Washington! I’d be happy to perform a custom equity study for you beyond the county information above and national figures below that is specific to your home’s specific features and today’s market trends.

Whether you own your home already or are considering building wealth through homeownership, I would love to help you analyze how equity growth and inventory levels could benefit your real estate goals. It’s always my goal to help keep you informed to empower strong financial decisions that augment your quality of life! Please reach out if you want to learn more.

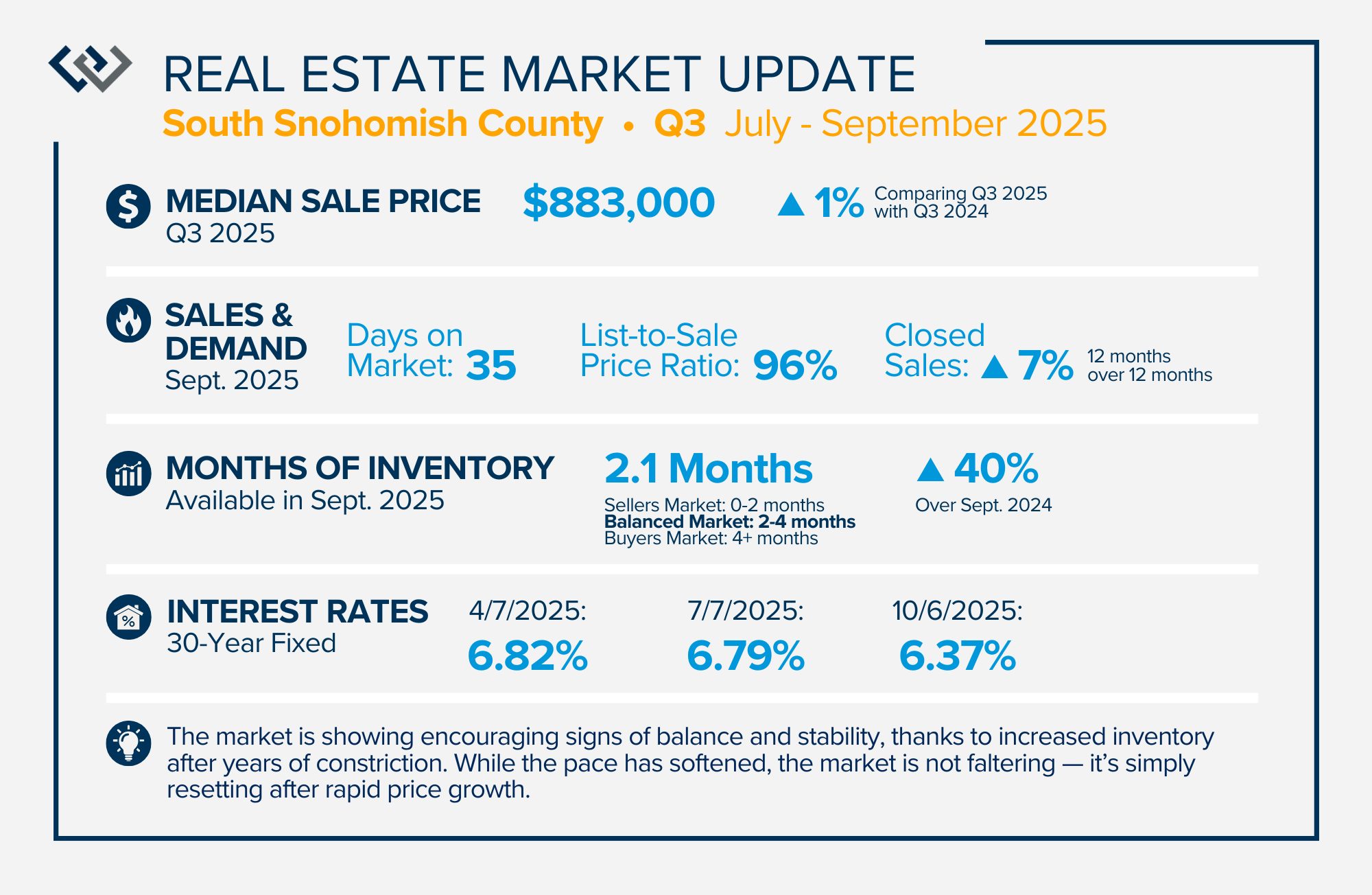

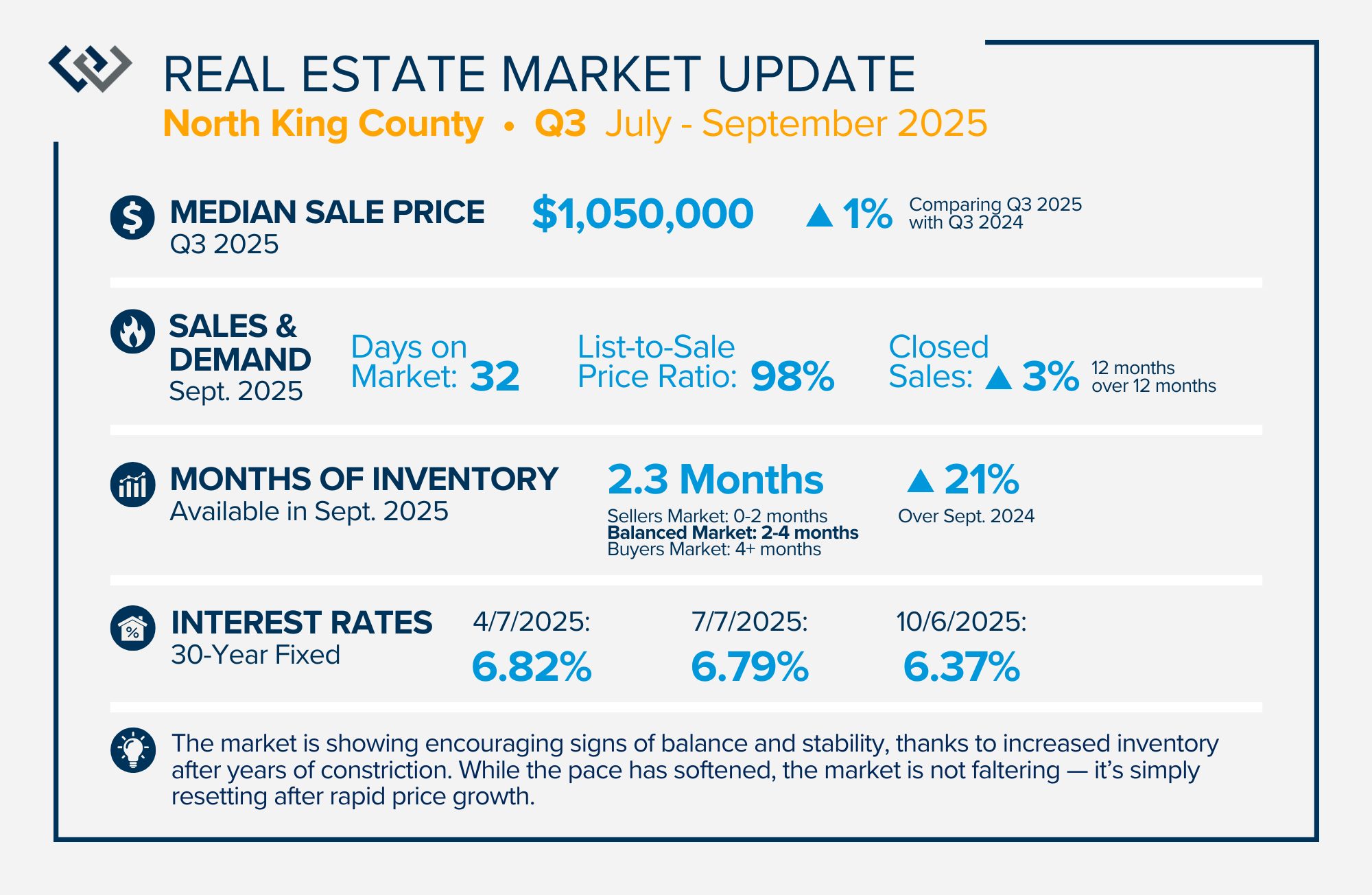

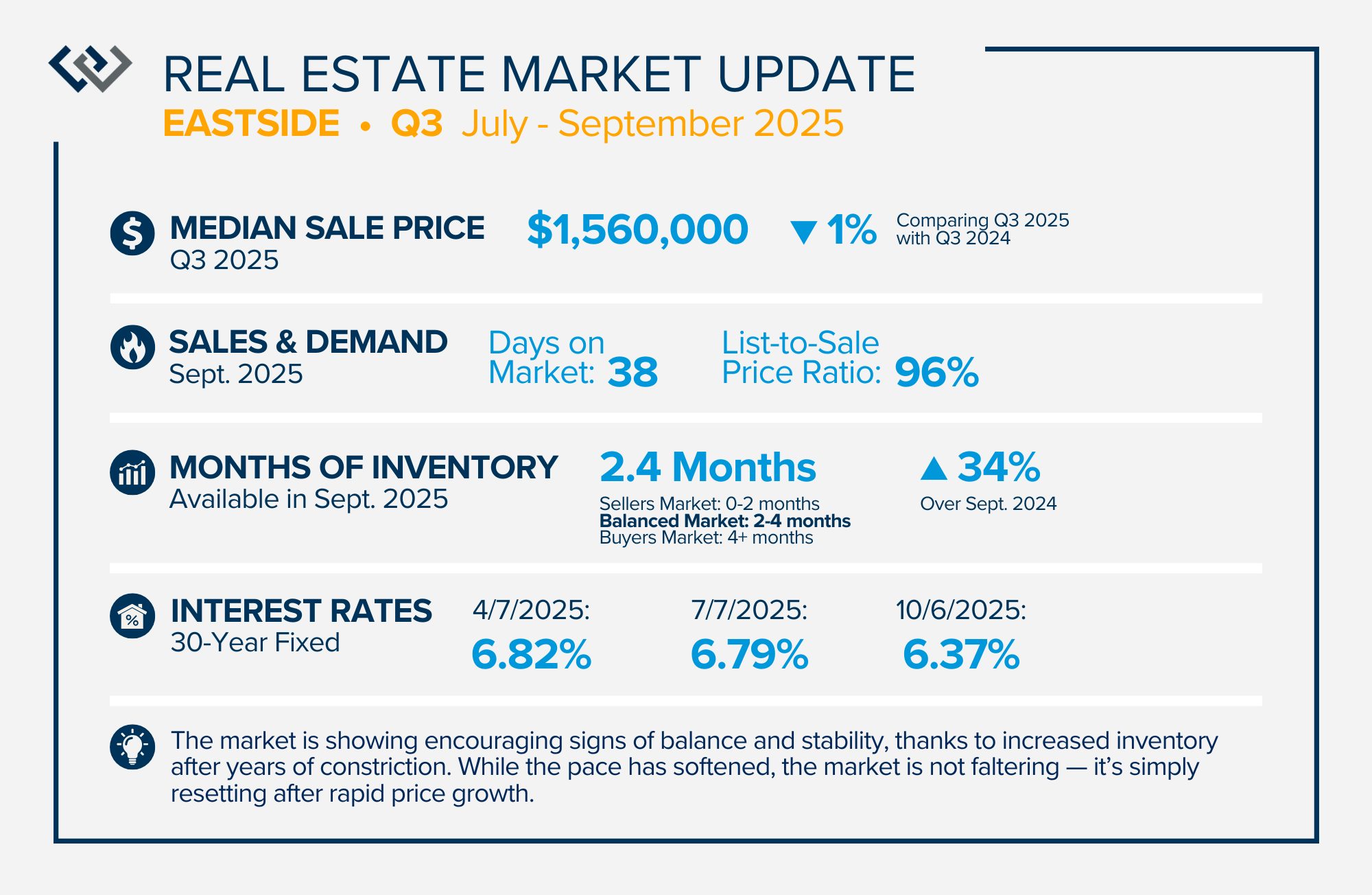

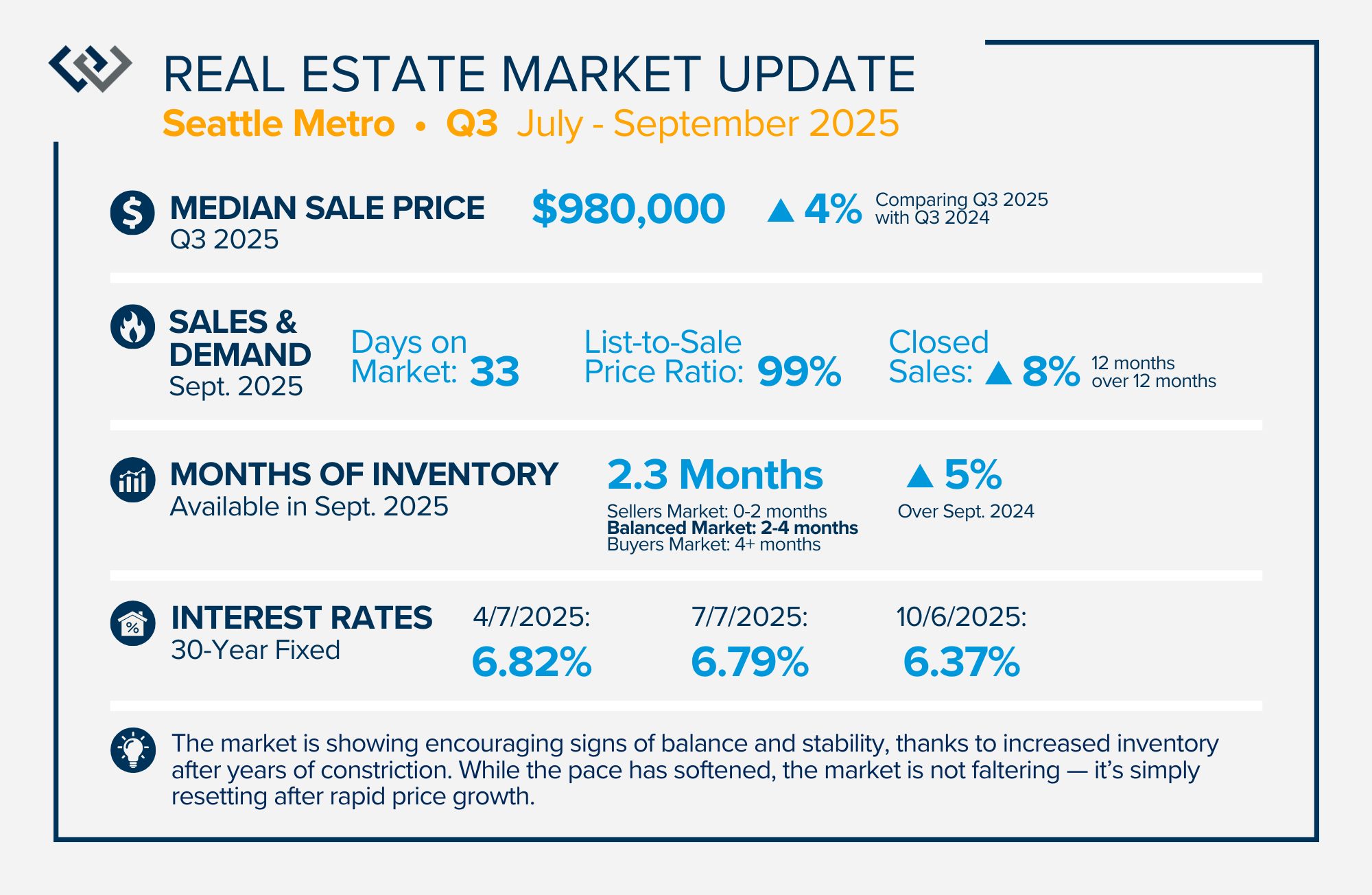

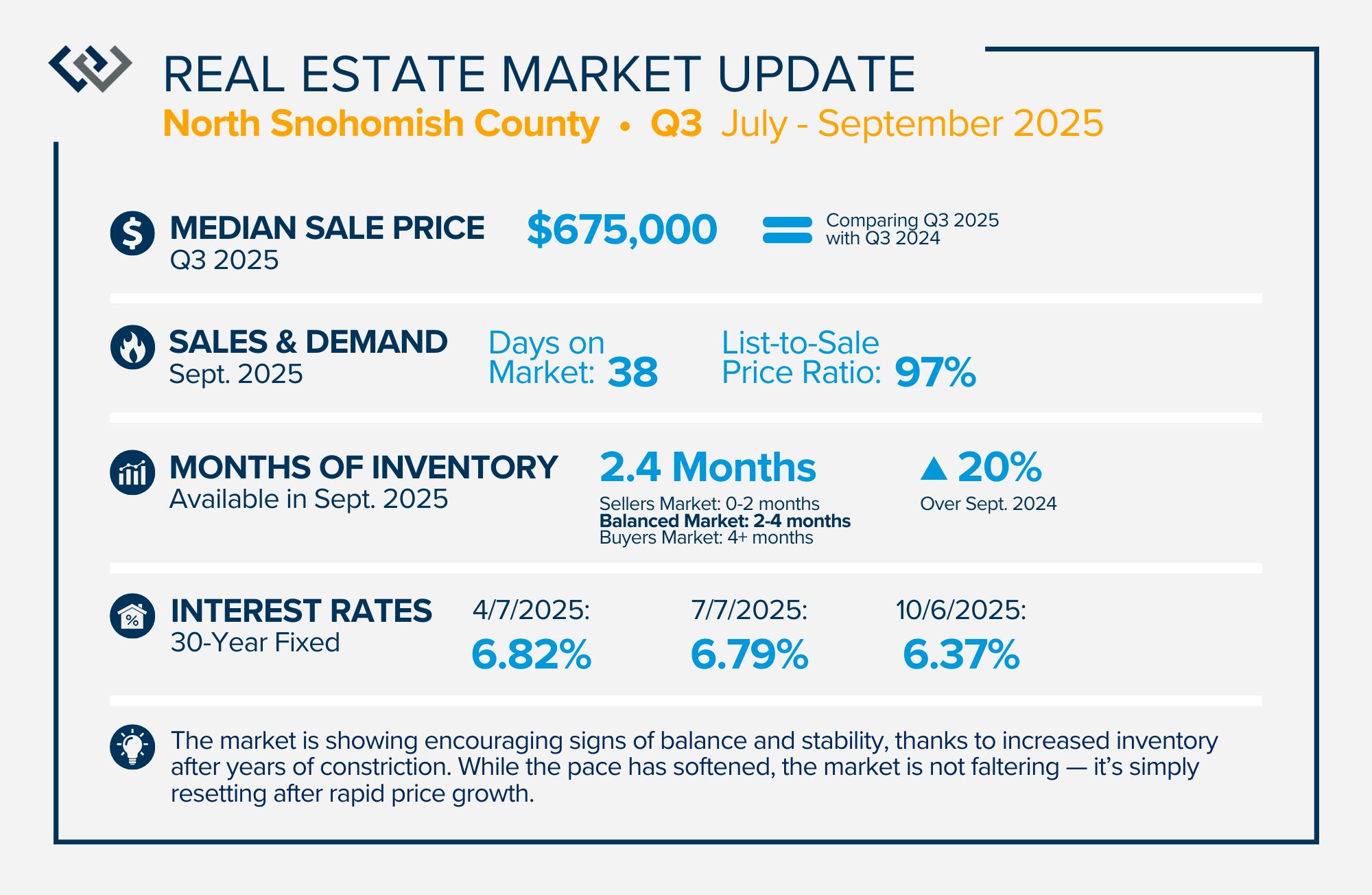

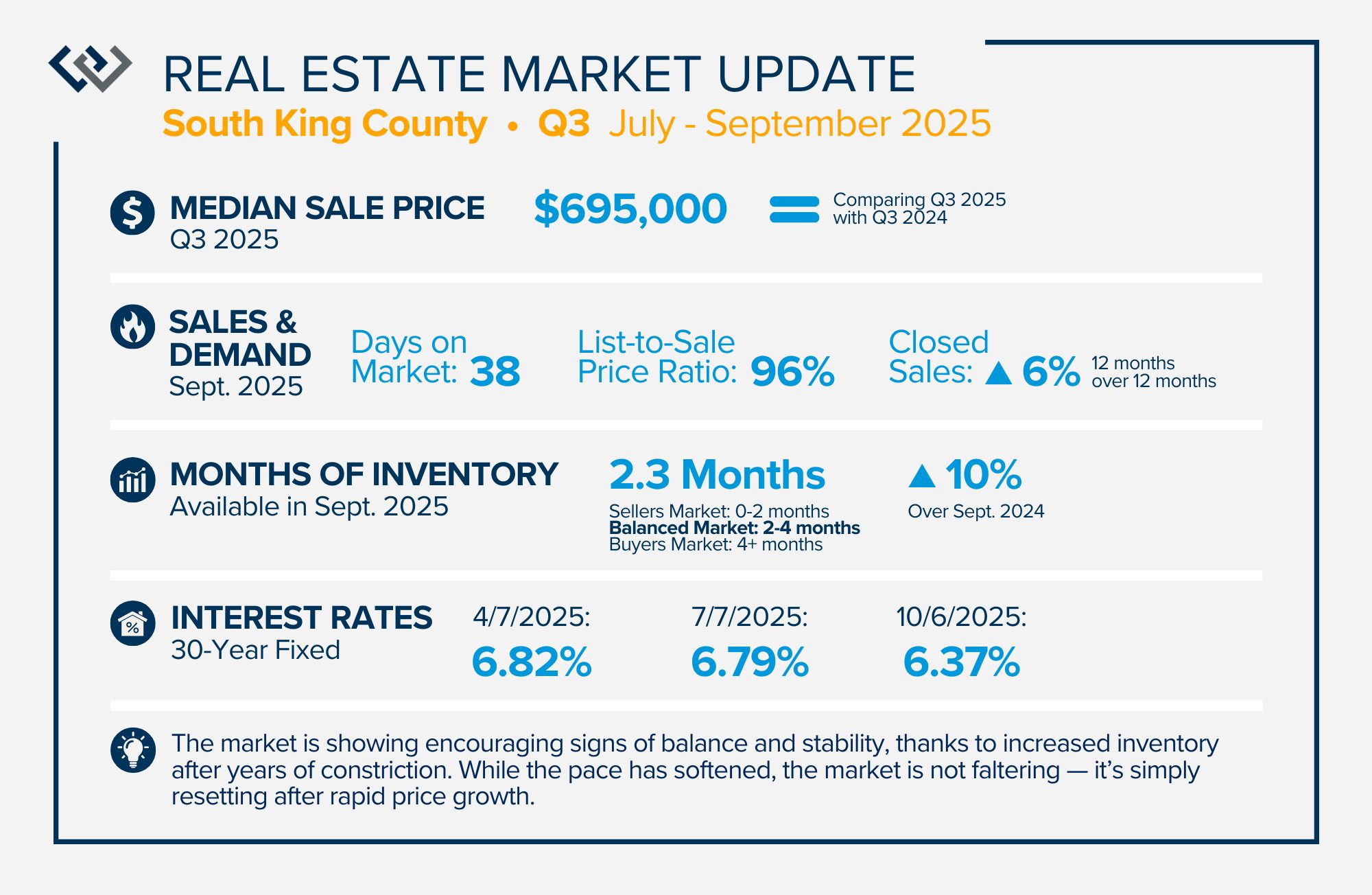

QUARTERLY REPORTS Q3 2025

The market is showing encouraging signs of balance and stability, thanks to increased inventory after years of constriction. While the pace has softened, the market is not faltering; it’s simply resetting after rapid price growth. Even with more homes to choose from, the median sale price remains steady year-over-year, and homeowner equity levels are at record highs.

More selection means sellers need to be intentional about property condition and pricing. Now, buyers have breathing room to make thoughtful decisions without frantic competition and are benefiting from easing interest rates and slower price growth.

For both sides of the market, the advantage now lies in strategy over speed. If you’re curious what this balanced environment means for your goals — whether buying, selling, or simply planning ahead — I’d love to talk through your options.

Data Over Drama: Why This Market Is a Reset, Not a Recession

The numbers tell us we’re steady, not sinking. Let’s replace uncertainty with perspective and see how stability sets the stage for opportunity and long-term success.

After years of rapid appreciation, the market is simply taking a breath. Prices are holding steady, inventory is at its healthiest level in over a decade, and interest rates are easing — all signs of balance, not decline. If you’ve been feeling uncertain about the housing market lately, you’re not alone. The media (news or social) loves drama, but the data tells a quieter, steadier story. What we’re seeing right now isn’t a recession — it’s a reset.

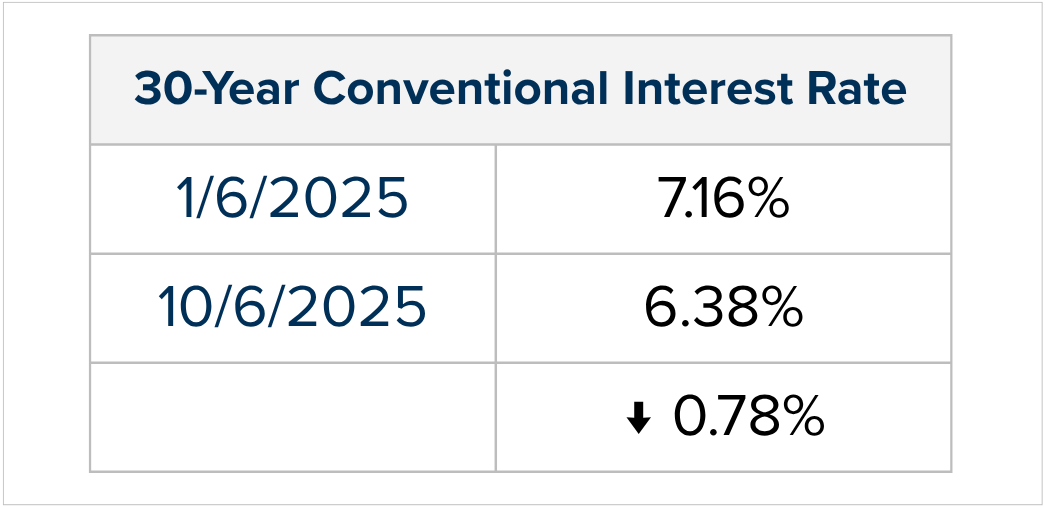

The combination of rates coming down by 0.78% since January 2025 and prices remaining flat year-over-year means that monthly payments for a new mortgage are starting to ease. This is a welcome trend for buyers who have been grappling with affordability. We’ve even started to see buyers who already own a home, willing to give up their lower rate to make moves to homes that better fit their lifestyle needs.

Another reason we are not in a recession is the abundance of equity many homeowners have. Median price in King County is up 33% since 2020 and up 98% since 2015. In Snohomish County, the median price is up 42% since 2020 and up 115% since 2015. During this time, prices grew quickly vs. the historical norms of 3-5% a year. Hence, prices remaining flat makes sense as the market levels out and finds its equilibrium. Further, according to Census data, a record 40% of Americans own their homes free and clear, the highest level recorded.

This kind of “flat” market often feels uncomfortable because it’s different from the fast-paced, multiple-offer environment we grew used to and found exciting. But in reality, flat doesn’t mean failure. It means opportunity — for buyers to make thoughtful moves without frenzy, and for sellers to position their homes strategically in a more stable environment and reap their well-established equity.

In my years of watching market cycles here in the Greater Puget Sound Area, I’ve learned that perspective is everything. For sellers, how long they’ve been in their home, assessing their equity level, and where they want to go are what matters most. A segment of the market that I’ve seen take a step back is speculative sellers hoping to buck the current trends and make a quick gain.

It is important to note that owning real estate is a long-term hold investment and not an overnight come up. The extreme ramp-up in home values from 2020-2022 skewed that viewpoint for some. A valuable rule of thumb to adhere to is the 5-year rule. Outside of the Great Recession of 2007-2012, holding for 5 years has overcome a flat market or any short-term dips in values. It’s also important to understand that your home serves two purposes: your safe place and an investment.

A home is surely an investment, but also a place to call home. It doubles as the place where one finds shelter, makes memories, and becomes a nest egg over time. It’s impossible to “time” the market! It’s more so about matching your home to your current needs, affording the monthly payment, and planning to stay awhile. With those three elements in mind, a successful investment will happen along with living in a home that aligns with your life.

For buyers, we haven’t seen this calm of a market environment and selection in ages. In our region, we are currently experiencing a balanced market (2-4 months of inventory). In some areas of the country, a balanced market looks different (3-6 months), but for our area, it’s tighter due to density, industry, and limited land availability.

While we do occasionally still see multiple offers, they are no longer the norm. Buyers are now afforded the benefit of longer market times, allowing for negotiated contract terms to support performing due diligence over a longer time. They also do not have to escalate as high in price to obtain a home. My hope is that buyers who have sidelined themselves or are considering a purchase realize that this is a great time to buy!

If you’d like to talk about what this balanced market means for your goals — whether it’s buying, selling, both, or just planning ahead — I’m here to help you make decisions with confidence. Following the news, doomscrolling, or listening to an isolated story could veil you from the truth the data provides. While the market might seem “boring” right now, I’ve seen many buyers and sellers find great success. Let’s talk and apply your goals to today’s trends!

Interest Rates Ease: Why Now is a Smart Time to Buy

Two unique opportunities have lined up for buyers:

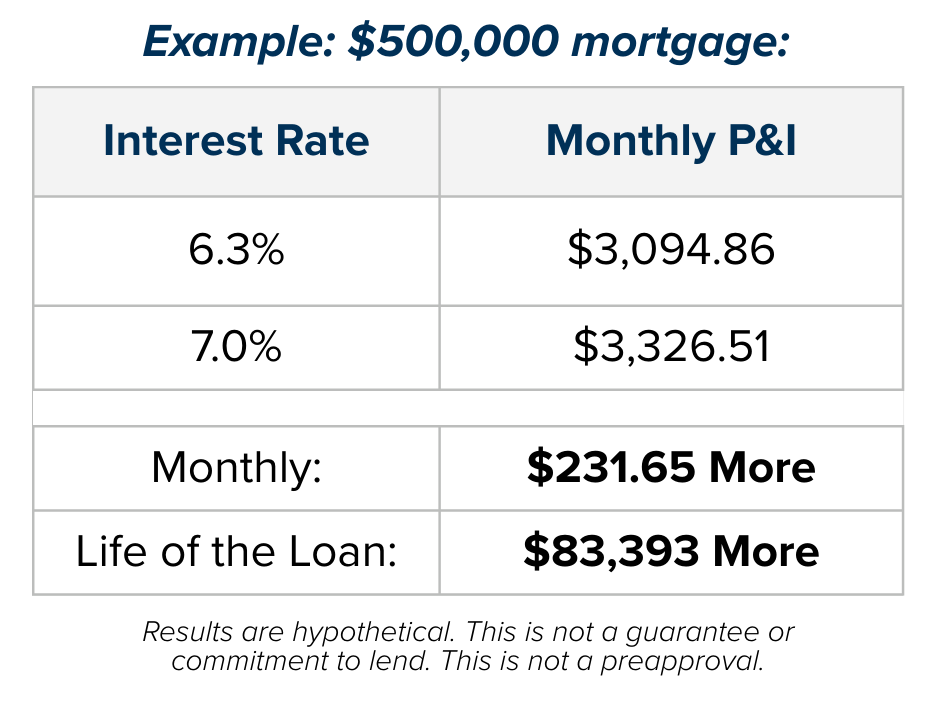

Lower Interest Rates – With rates down almost three-quarters of a point, a $500,000 mortgage costs $232 less per month than it would have just a short time ago. That’s nearly $84,000 saved over 30 years.

More Homes to Choose From – We’re seeing the highest inventory in 14 years, giving buyers more options, less competition, and greater negotiating power.

Why this makes it a good time to buy:

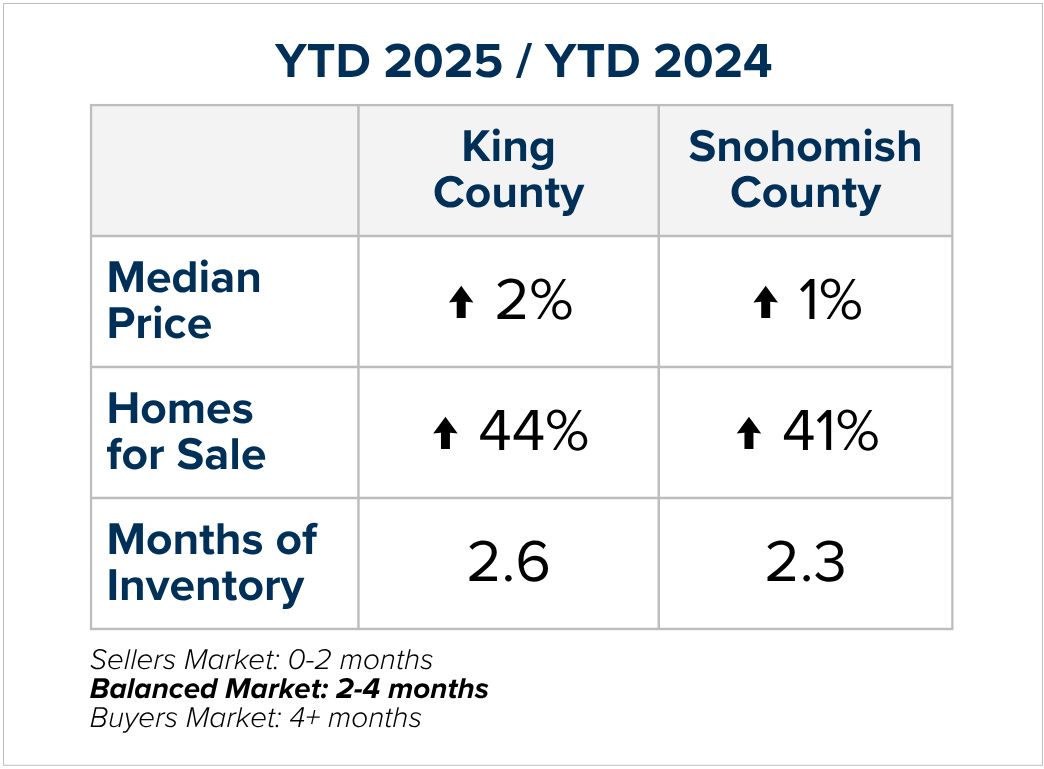

Opportunity to Build Wealth – Prices are up 2% in King County and 1% in Snohomish County year-over-year and if rates continue to soften, prices will rise. Fixing your price now will lend itself to great, long-term equity growth. In fact, homes in King County are up 33% over the last 5 years and up 80% of the last 10 years. They are up 42% in Snohomish County of the last 5 years and up 98% over the last 10 years.

Find the house that best suits your life – Moves are brought on by life changes. If you see yourself entering a new chapter, whether it is joy-filled or challenging, a purchase can help align your home with your life. Pause to assess if now would be the right time to make a move and consider the advantages of the current market.

All of this means more affordability and more choices—a rare combination in real estate. Please reach out if you would like to learn more. It is my goal to help keep my clients informed so they are empowered to make strong decisions.

Power Shift: Increased Selection, Interest Rate Stability, and Tempered Price Growth give Buyers an Edge

2025 has been the year of a power shift in the real estate market, as we experience more balance in the market. Increased inventory has provided the biggest advantage for buyers, giving them more selection, which has tempered price growth and aided affordability. In King County, there were 43% more available listings in July 2025 over July 2024, and 47% more in Snohomish County. This, along with the new normal of interest rates, has buyers who are ready to make a move in a positive position to pounce. We have even seen rates come down close to 6.5% for a 30-year conventional loan and to 6.15% for FHA and VA loans in the last two weeks!

Surprisingly, as we find ourselves in the dog days of summer with many people enjoying the last bits of kids being out of school, taking vacation time, and savoring all the PNW has to offer during the summertime, we have seen buyer activity start to increase. Month-to-date this August, pending sales are up over July 2025 by 9% in King County and up 17% in Snohomish County. This is on the heels of pending sales leveling out in King County in July 2025 over June 2025 and increasing by 12% in Snohomish County. With 36% more homes for sale in King County YTD and 41% more in Snohomish County, buyers are starting to understand the opportunity increased selection brings. According to the Mortgage Bankers Association (MBA), mortgage applications are also up year-over-year.

The increased selection has created more room for buyer negotiations and further opportunity to perform due diligence. Compare this to the previous onslaught of bidding wars, buyers now have a calmer environment to make big decisions. We have even seen the return of successful home sale contingencies when the right situation presents itself. Basically, the market has become more fluid and less of an uphill battle for buyers to secure a home. Evidenced by the average list-to-sale price ratio for a home in King and Snohomish Counties in July, at 98%. Last July, when there was less selection, the average list-to-sale price ratio was 100% in King County and 99% in Snohomish County. With that said, we are still seeing homes that are brought to market that are well priced and in prime condition getting multiple offers and selling for over list price. It is just no longer the norm and more so the exception.

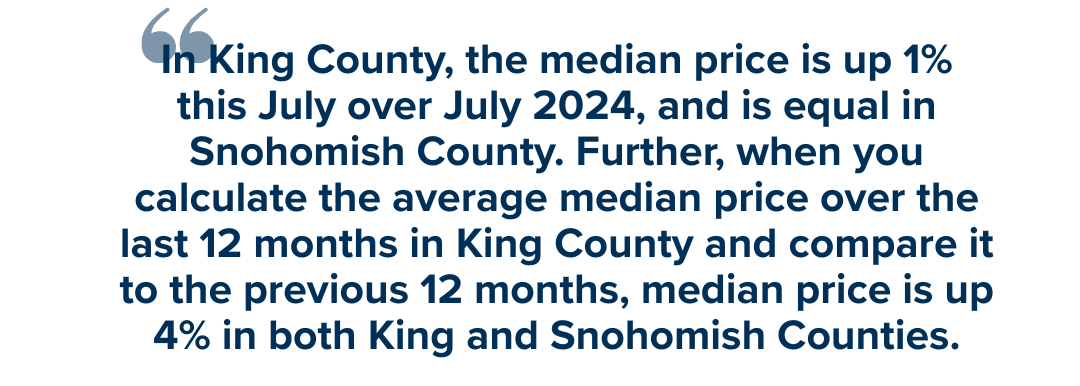

This has resulted in median price growth becoming flat, but not faltering. In King County, the median price is up 1% this July over July 2024, and is equal in Snohomish County. Further, when you calculate the average median price over the last 12 months in King County and compare it to the previous 12 months, median price is up 4% in both King and Snohomish Counties. We are nowhere near a free fall in prices; what we are experiencing is a deceleration in price growth. Since this has followed the unprecedented double-digit, year-over-year price growth we saw during the pandemic, some may see this as the sky is falling, which is simply wrong. This is a good thing!

The abundance of equity that was gained over the last five years and certainly over the last decade has many sellers making great gains. Median price in King County, including single-family residential homes and condos, is up 31% since 2020 and up 73% since 2016; and in Snohomish County, it’s up 40% since 2020 and up 99% since 2016. Bear in mind, real estate is a long-term hold investment, and timing a sale after the original purchase can have an impact. We are seeing many Baby Boomer sellers start to make big moves towards retirement, enjoying their well-earned financial freedom and, in some cases, addressing health needs. The move-up buyer/seller is returning to the market as well, putting their equity to work for them to purchase a home that better fits their household size and preferred location.

With interest rates predicted to only slowly recede, some buyers are using negotiated credits to buy down their interest rate and decrease their monthly payments. Buyers who are finding a way to make the monthly payments work, either through buy-downs or budgeting, are getting themselves into homes that feel better for their lives. They are also setting themselves up for long-term gains as their nest egg grows while they enjoy their home. It is important for everyone to understand that real estate is not typically a quick come-up investment. The pandemic years skewed that perspective, and returning to more historical norms should be welcomed, as that growth was unsustainable.

If you have been considering a move or know someone who is, now is a great time to consider your options and start planning. We have even seen first-time home buyers eager to jump into the market and start building wealth. I could easily apply the statistics above to your specific location, and we can apply the market conditions to your goals. Meeting up in person or via Zoom to discuss what this market has to offer and answer your questions is the foundation of my service. It never hurts to dream, plan, and discuss whether your desired outcome results in doing something sooner or later. This consultation meeting will lead to confident decision-making based on clarity and trust. It is a positive and proactive step forward, and is always based on the pace of my clients’ wants and needs. It is my goal to help educate in order to empower strong decisions. Please reach out if you want to chat about how your goals align with today’s market or if you know someone who could use this counsel.

When it’s Time to Move on to the Next Chapter: A Guide for Baby Boomers and Their Families

In 2025, we have seen a year-over-year increase in new listings. New listings are up 16% in King County and 10% in Snohomish County, following a 19% increase in King County and an 18% increase in Snohomish County in 2024 compared to 2023. This mounting increase piqued my curiosity, and I began to notice some trends in the inquiries that were coming my way. The trend involved Baby Boomers being on the move!

Baby Boomers account for 21% of the US population and are now in their 60s to early 80s. This is a large group navigating major life changes. With fewer encumbrances and responsibilities, many see this as an incredible opportunity to explore their freedom and financial stability. It’s their time! Some are also slowing down, possibly facing challenges, and are seeking comfort and assistance. Many Baby Boomers are moving out of their longtime homes and choosing to reposition either in the same area or out of state. They are buying their dream home that aligns with their lifestyle (think snowbirds), downsizing to a condo or small rambler, moving in with or near family, or relocating to a retirement community, and in some cases, an assisted living facility. The good news is that this generation is sitting on a substantial amount of home equity that is fueling these moves and providing the means to achieve their goals.

The average Baby Boomer has owned their home for 17-23 years and has 60-80% home equity, and in many cases, owns their home free and clear. In May 2025, the median price for a single-family residential home in King County was $865,000, and $785,000 in Snohomish County. That is a 127% increase in King County over 20 years and 162% increase in Snohomish County. This nest egg is providing Baby Boomers the financial flexibility to move to a place that will bring peace, ease, and enjoyment in their next chapter.

Deciding to sell a longtime home is never just about real estate—it’s about life, legacy, and letting go. For many Baby Boomers, the idea of moving can bring up a flood of emotions, logistical hurdles, and financial questions. As a real estate professional who has worked with many beloved clients in this exact stage of life, I want to offer some guidance—not just as a broker, but as someone who deeply cares about helping people make this transition with grace and confidence. Whether you’re considering a move yourself or you’re supporting a parent or loved one through this decision, here are some of the biggest challenges we see—and some helpful ways to navigate them.

Fearing the Unknown

Change is never easy, especially when it means leaving behind a familiar neighborhood or lifestyle. There’s often a real fear about what the next step looks like.

What helps:

Take your time exploring options. Visit potential new homes or communities before making a decision. Think about what you want out of life: less upkeep, more walkability, or being closer to loved ones. Often, the move brings more peace, not less. It’s the transition that can be stressful and intimidating, but the end result is worth the temporary discomfort.

Letting Go of a Lifetime of Memories

Your home holds decades of family stories. Maybe it’s where you raised your children, loved your pets, celebrated holidays, or shared countless quiet mornings. The thought of saying goodbye can feel overwhelming.

What helps:

Consider reframing the move. You’re not erasing memories—you’re making space for a new chapter. Think of it as passing the home on to a new owner who will love it just as much. Many clients find comfort in creating photo albums or video tours to preserve those meaningful memories.

Facing the Overwhelm of What to Do with Your Stuff

Sorting through years (or decades) of belongings is one of the biggest roadblocks. It’s easy to get stuck when everything feels important.

What helps:

Start small. Focus on one room at a time, and prioritize the items that hold true sentimental value. Enlist a senior move manager or downsizing expert who specializes in this type of transition. Their help can make the process feel more manageable—and far less emotional. I have contacts for professionals who specialize in these services, whether it is sorting and packing or estate sale assistance, I can connect you with trusted service providers.

Managing the Physical Demands and the Time Suck of a Move

Packing and moving can be tough at any age, but especially so for those with mobility issues or health concerns. Furthermore, if you are still working and have a busy schedule, a move can seem out of reach.

What helps:

This is the time to lean on help. There are incredible services available that handle packing, organizing, moving, and even estate sales. Make sure the new space is designed with safety and comfort in mind—single-story homes, walk-in showers, and easy access all make a difference. This move is an opportunity to have your home align with exactly what you need and want to thrive.

Navigating the Financial Piece

Worries about affording a new place—or not getting full value from the home sale—can keep people stuck.

What helps:

Work with a trusted real estate broker, CPA, and financial advisor who understand your goals, tax code, and the current market trends. Many of my Baby Boomer clients are surprised to learn how much equity they’ve built over the years. That equity can open doors—to a smaller, more manageable home, a lifestyle upgrade, extra savings, or even travel or care options you’ve been dreaming about. Also, if you plan to apply for a mortgage and are approaching retirement, you’ll want to strategize with a reputable lender on whether it makes sense to make your move while you’re still working or after you retire.

Access to Financing Options for My Next Purchase

Once retired, many Baby Boomers are unsure how to finance their next move, especially if the majority of their cash is tied up in the equity of their current home.

What helps:

Accessing your equity to pay for your next place, so you don’t have to move twice or make a contingent offer. Often, properties that appeal to downsizing Baby Boomers are highly sought after, and home sale contingent offers struggle to compete. Utilizing a bridge loan eliminates the need to be contingent, gives you access to a large amount of your equity, and lets you secure your new place before having to sell your current home. Windermere has an excellent Bridge Loan Program with quick approvals that don’t require an appraisal, and no fees are collected until your home sale is closed, eliminating up-front out-of-pocket expenses.

My House Needs Some Work, and I Don’t Have Access to Money

Maintaining a house requires keeping up with deferred maintenance and making home improvements. These costs can be tough when on a fixed income. Maybe a refresh of a kitchen or bathroom would result in you getting more money for your home when you sell.

What helps:

Have your trusted real estate broker weigh in on your home’s condition and what improvements create the highest return. Windermere also has a loan program called Windermere Ready that allows homeowners to easily access their equity for home maintenance, improvements, and moving expenses. Like the Bridge Loan, the turnaround time is quick, and there are no upfront fees.

Final Thoughts: It’s Okay to Take Your Time

If you’re reading this and feeling a mix of excitement, hope, and some uncertainty—you’re not alone. Selling a long-time home is a major life milestone. But with the right support, it can also be an exciting fresh start.

If you or your loved one are starting to explore this idea, I’m here to talk—without pressure or timelines. My goal is to equip you with tools and guidance to help you feel confident, informed, and cared for, every step of the way.

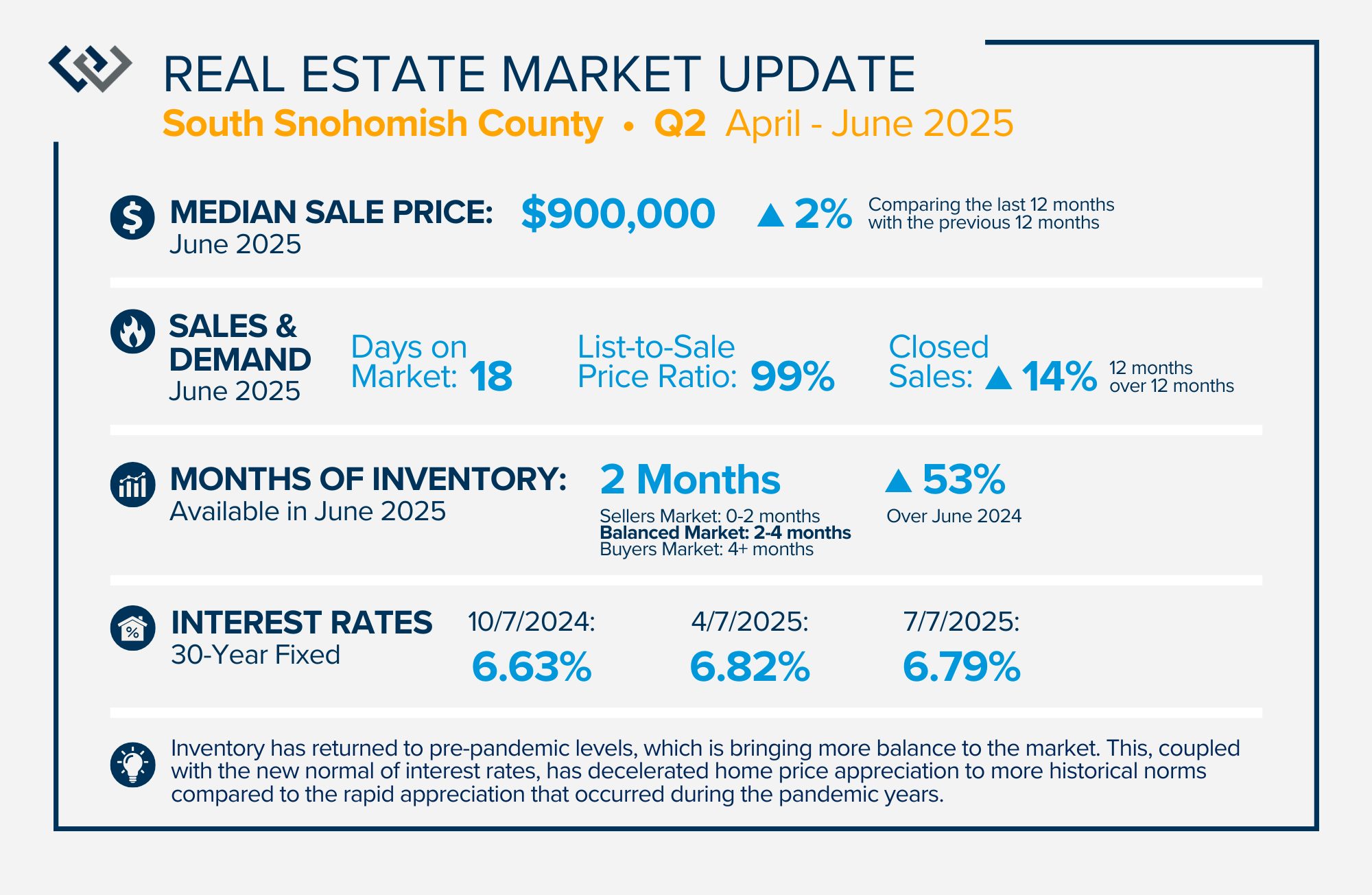

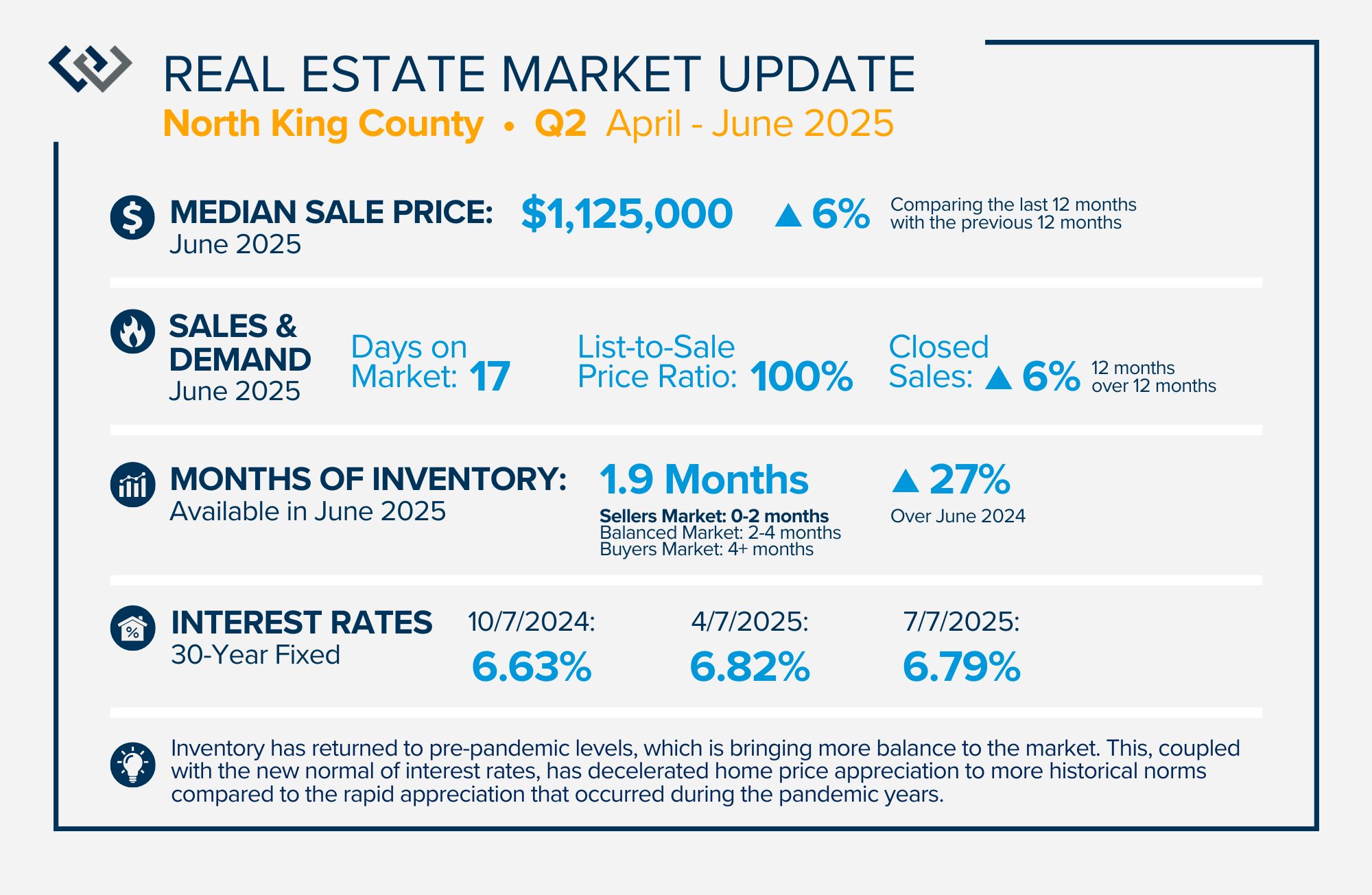

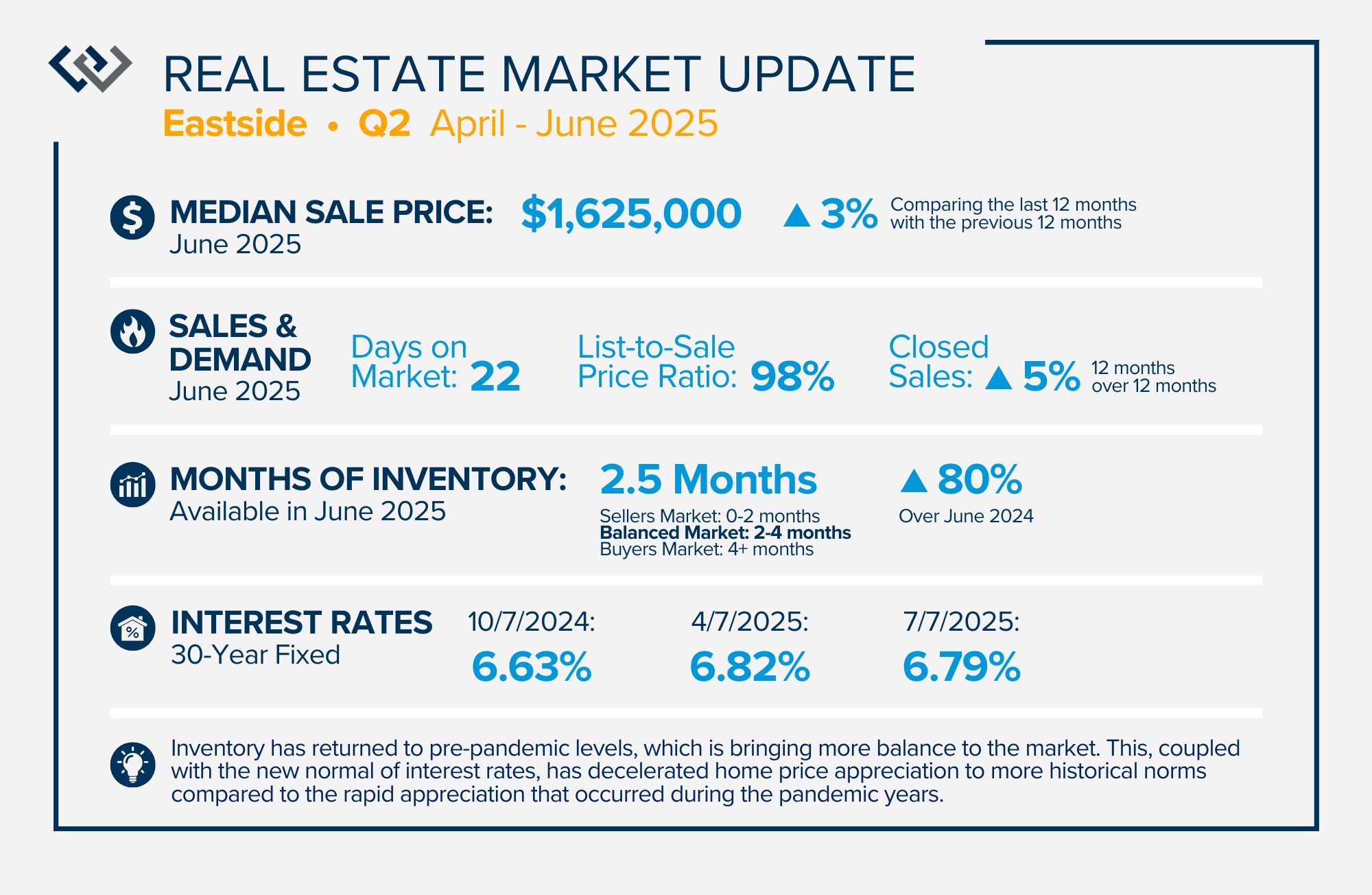

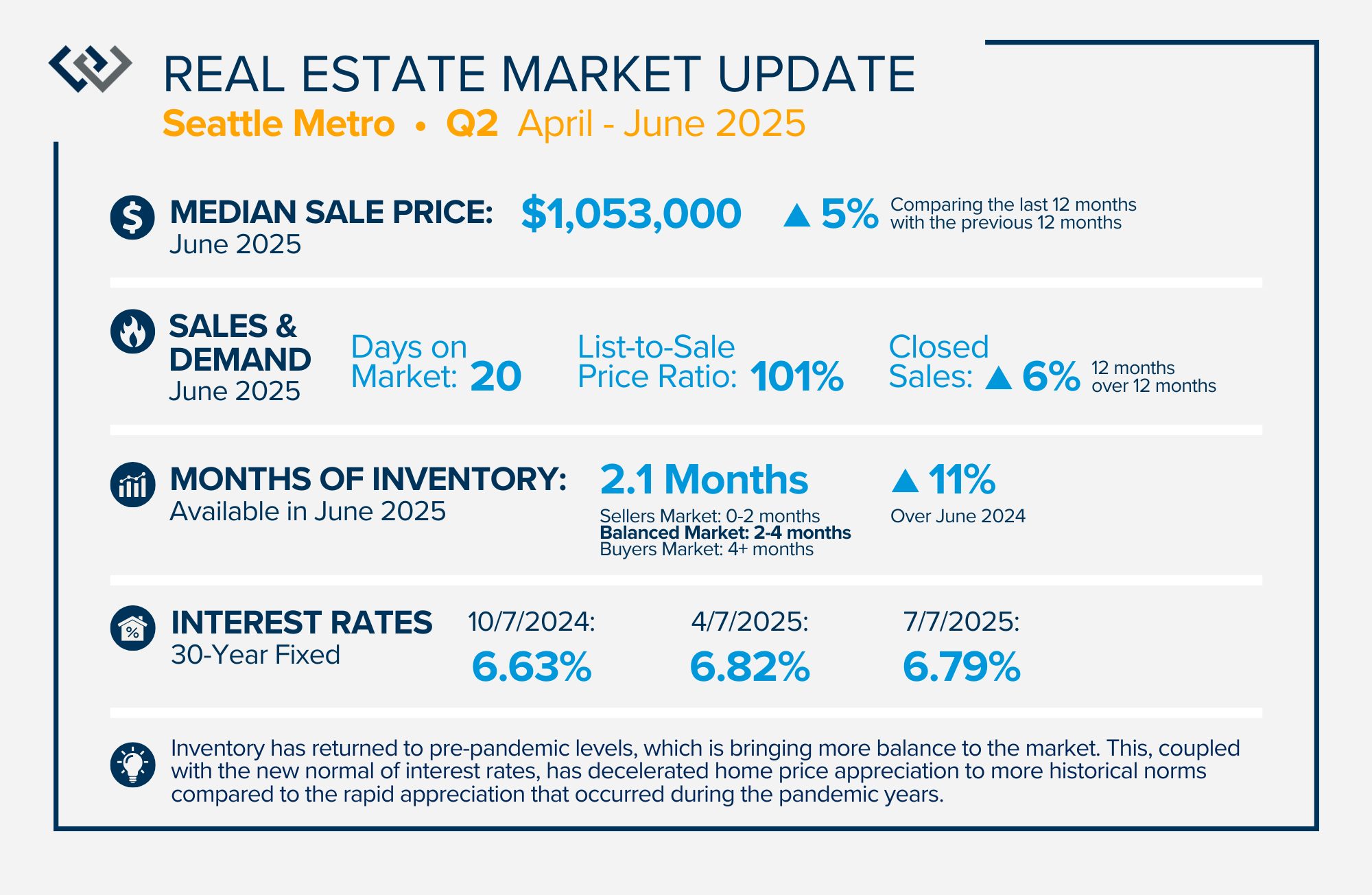

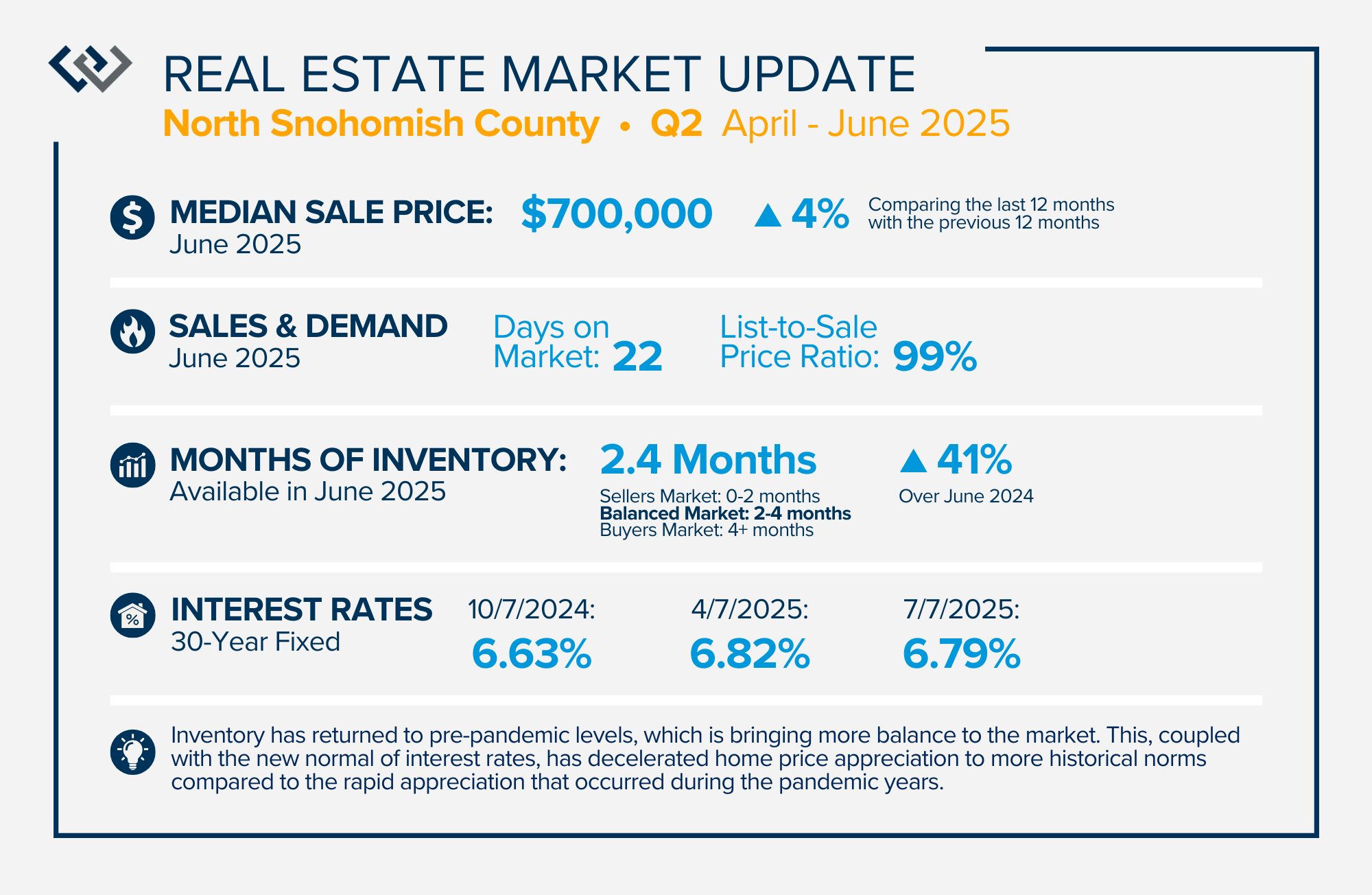

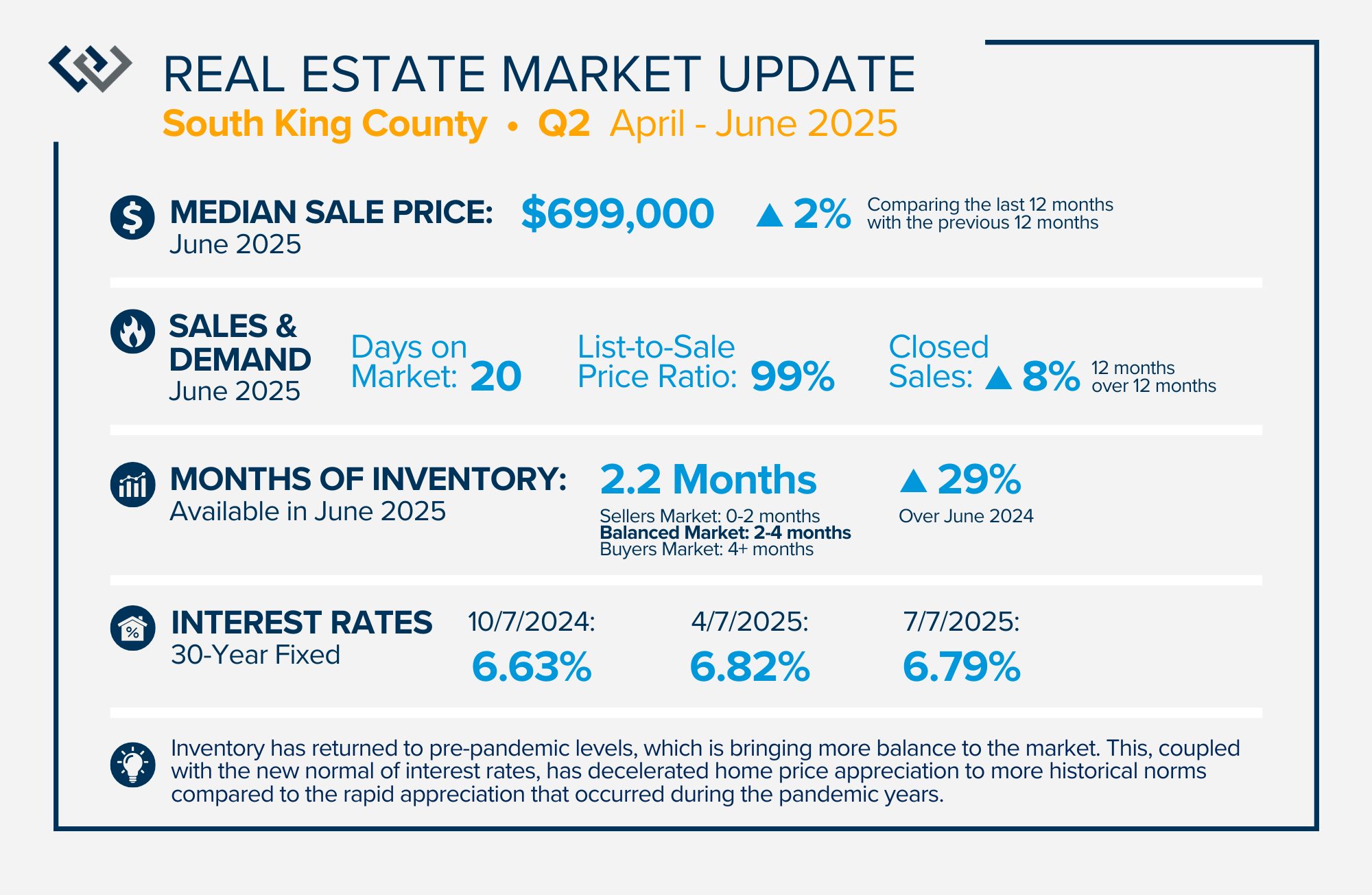

QUARTERLY REPORTS Q2 2025

The second quarter of 2025 had a significant increase in the number of available homes for sale. Inventory has returned to pre-pandemic levels, which is bringing more balance to the market. This, coupled with the new normal of interest rates, has decelerated home price appreciation to more historical norms compared to the rapid appreciation that occurred during the pandemic years.

Overall, equity levels are high, and sellers who have owned their homes for five years or more are making substantial returns. With more balance in the market, buyers are experiencing relief and new opportunities. Movement in this market is much more fluid than in the restricted inventory market. If you or someone you know is interested in learning more about how the current trends relate to your goals, please reach out.

PROPERTY CONDITION MATTERS: Two Exclusive Equity Loan Programs for Windermere Clients Listing Their Homes

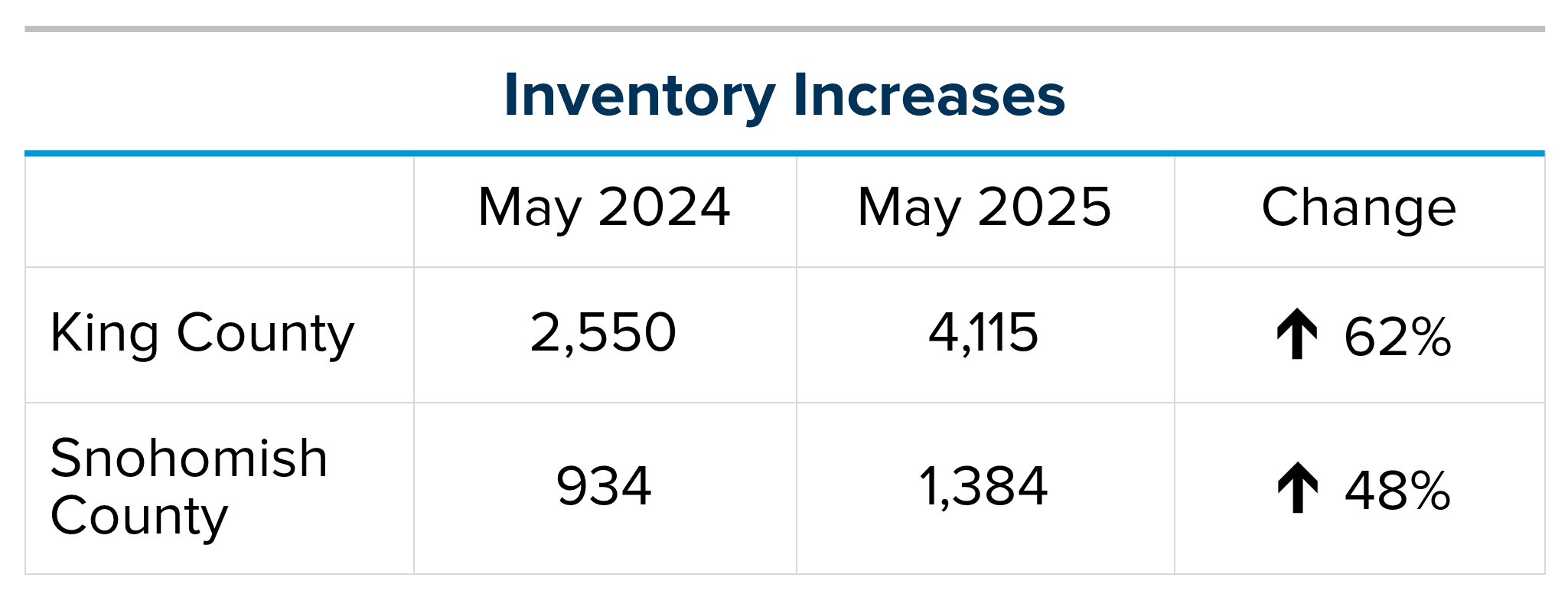

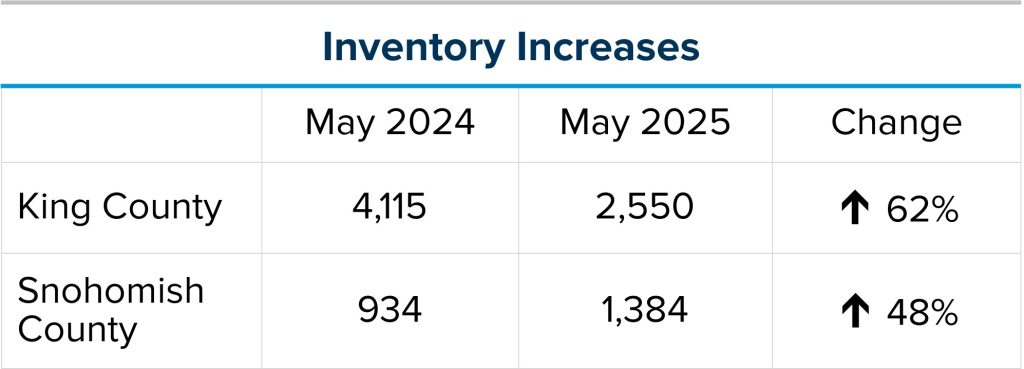

As market conditions shift and inventory increases, we are seeing that homes brought to market with sound property maintenance and thoughtful improvements are selling the fastest and yielding the highest returns. Inventory is up 62% year-over-year in King County and 48% in Snohomish County, highlighting the importance of standing out amongst the crowd. With interest rates remaining stubborn, monthly payments are buyers’ biggest concern, and many do not have the funds to make necessary repairs and improvements after a purchase. Eliminating property condition hurdles and even making modern improvements before listing the home is key to a seller’s success in getting their home sold!

Hurdles that we often encounter, which can adversely affect a home’s marketability, include deferred maintenance such as paint, carpet, and system improvements to HVAC, electrical, and plumbing systems. If a house needs a new roof or another central system replaced, this helps mitigate the upfront out-of-pocket expense. We have also seen sellers remodel and update areas of the house, such as the kitchen and bathrooms, to modernize and appeal to a broader audience. Exterior landscaping and junk hauling are also areas that help properly prepare a home for the market. A seller-procured pre-listing inspection often guides these improvements.

This is why Windermere offers two exclusive loan tools to provide sellers with access to funds based on their equity, helping them prepare their properties for today’s market. This approach is more efficient than wading through the red tape and longer timeframe associated with opening a Home Equity Line of Credit (HELOC). The Windermere Ready Loan Program now has two loan programs.

The first program ranges up to $50,000, and the second one ranges from $50,001 to $100,000. Funds for the first program can be available to the homeowner as soon as the same day the application is processed (within minutes), and the second program loans are funded within 10 days of application approval. Approval for both loans are based on the homeowner’s credit score rating and the Windermere broker’s approval of the home’s market value to establish equity within the required loan-to-value ratios. There is no need for an appraisal; both programs provide home sellers quick and easy access to funds via a loan against their equity. Then they can get to work preparing their homes for sale to attract the largest possible buyer audience.

The home equity serves as the basis for these loans, so it does not require employment verification, making this an excellent option for retirees or sellers in a job transition. Over 50% of all homeowners in the US have equity of 50% or more, making this tool the perfect solution to help would-be home sellers prepare their homes for the market and appeal to as many buyers as possible. Plus, there are no up-front costs; the loan fee and accrued interest are paid off at closing.

So, how do these programs work? First things first, contact me, your Windermere broker, as these programs are exclusive to Windermere brokers and their clients. We can evaluate which areas of improvement will yield the greatest return based on market data and trends, establish a budget with bids from my trusted vendors, and devise a winning strategy.

In the meantime, if you want to learn more about how home improvements can help maintain and enhance a home’s value, check out the 2025 Remodeling Impact Report from NAR. This will provide valuable insight. As always, my goal is to help keep my clients up-to-date on the latest trends and empower them to make informed decisions.

My office just had our annual Community Service Day, where we worked with the Snohomish Garden Club, prepping, planting, and working hard to help make sure our local food banks will get thousands of pounds of fresh produce for our neighbors in need.

This is just a piece of the larger puzzle of Windermere’s commitment to community, and my office’s commitment to take on local projects.

Thank you for choosing Windermere and helping make all of this possible!

Change is Inevitable, Find the Opportunities in the Shift

The headlines are swirling about the real estate market. The environment is shifting from a seller’s market to a balanced market, creating opportunities for buyers and holding sellers to exacting standards. The primary factors affecting this shift are inventory levels, interest rates, and consumer confidence. These are the same factors that commonly influence the market conditions, and for the first time since 2018, months of inventory have reached their highest peak. Interest rates have remained stubborn, hovering around 7% for the last six months, and the stock market drama in April took a toll on consumer sentiment.

The good news is that the stock market has fully recovered from the April decline; however, the residual effects are likely to have some lasting impact on consumer confidence as they plan their financial decisions. Other good news for buyers is the increase in selection, which allows for more negotiations and can provide the option of a buyer credit. In King County, there were 62% more homes for sale in May compared to the same month last year, and 33% more than in April. In Snohomish County, there were 48% more homes for sale in May compared to the same month last year, and 32% more than in April. It is also important to note that each sub-market, established by price point, location, and property type, can vary. We are currently seeing a mix of sellers’, balanced, and buyers’ markets across the region as inventory increases.

We surveyed our office’s pending sales over the last two months, and one in three transactions had a buyer credit, with an average credit of $14,000. This is where a credit to the buyer from the seller is baked into the contract. Often, this accompanies a full-price offer (from the list price), and sometimes the offer is below the list price. These credits are used to offset the buyer’s closing costs, which leaves more money in the buyer’s pocket post-closing for improvements, a larger down payment, or savings. We are also seeing savvy buyers use these credits to buy down their interest rate, thereby saving on their monthly payment.

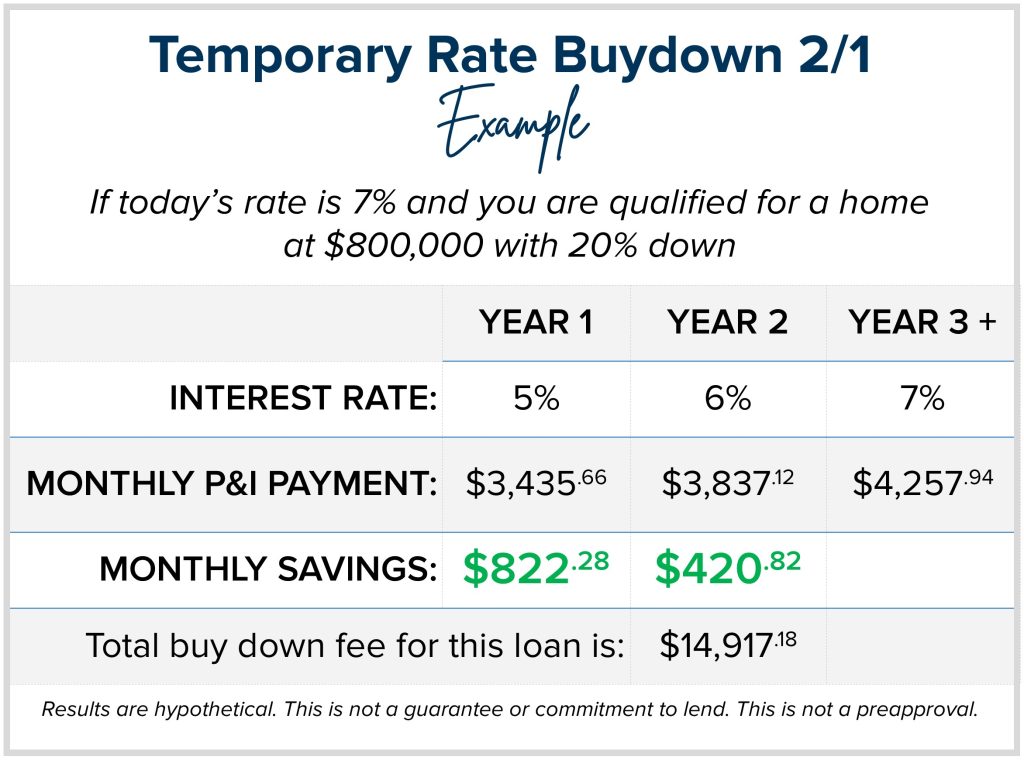

A permanent rate buydown requires approximately 3% of the purchase price to lower the rate by one point for the 30-year term of the loan. A good rule of thumb to remember is that every 1-point decrease in rate equals a 10% increase in buying power. For example, if the rate is 7% and you are qualified for a home at $800,000, and the rate were to decrease by 1 point to 6%, you could now afford $880,000 with a very similar payment. Another way to look at this is simply the monthly payment itself. An $800,000 purchase with 20% down and a 6% interest rate would save a buyer $420.82 a month compared to the payment at 7%.

A permanent buydown is a valuable tool, as is a temporary buydown. It is one of the most powerful tools in today’s market. It costs far less than a permanent buy-down. Here is an example: let’s say you are shopping for a house and have an $800,000 budget, along with a 20% down payment (btw, this works for any down payment amount), given today’s interest rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2), which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

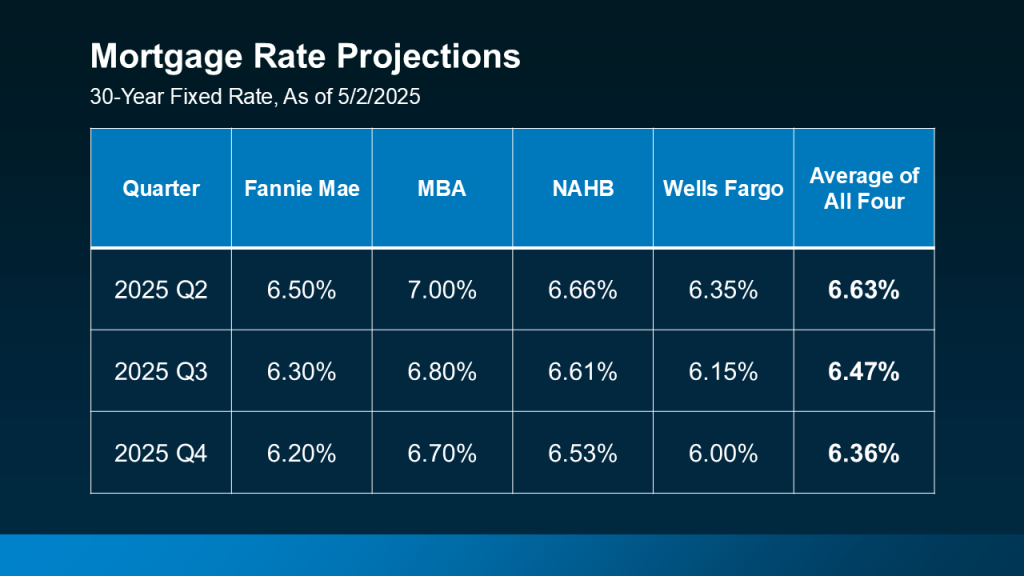

The roughly $15,000 in monthly payment savings is paid upfront at closing and can be provided as a buyer credit by the seller. The buyer still needs to qualify based on the 7% interest rate, as the payments will be converted to those based on the 7% rate in year three and moving forward. The buyer may never have to pay the 7% amount if rates decrease and they can refinance within the two years, permanently locking in a rate below 7%. A bonus is that if the entire $15,000 credit has not been used yet, in some cases, those unused funds can be applied towards the refinance. The latest expert rate predictions are below. While we don’t have a crystal ball to predict when this will happen, I do know that when it does, there will be more buyer competition in the market, which will affect negotiations.

A peculiar aspect of consumer sentiment is that when there is more inventory and the market becomes more balanced, as opposed to a tight market where buyers are competing for limited choices, it confuses buyers. They tend to slow down and think something may be wrong. Savvy buyers will zero in on a house they want and use this time to negotiate better terms for due diligence and possible credits, rather than escalating prices and accepting no contingencies that often occur in a seller’s market. Another benefit to a balanced market is the return of home sale contingencies. This balance of inventory is necessary to introduce this option, and it has been quite a while since we’ve seen this happen. Although they are not commonplace, they are on the rise. This enables the buyer to purchase contingent on the successful sale and closing of their current home. It was how real estate used to be done, and a great option if all lines up.

Now, how does this increase in inventory affect sellers? As mentioned above, it raises the bar on property preparation, accurate price positioning, and overall appeal. When there are more choices, you need to stand out! That is why homes that meet these criteria continue to sell for more than their list price and receive multiple offers. Homes that are brought to market, neutralized, staged, free of deferred maintenance, and appropriately priced are selling quickly. If a home has modern improvements, that helps too, as many buyers prefer move-in condition as they are often using the bulk of their savings for a down payment to create the lowest possible monthly payment.

So, what is appropriate price positioning? I will start with the big picture first. Sellers must maintain a long-term perspective and assess their equity growth during their ownership. Single-family residential prices in King County have increased by 91% over the past decade and by 44% over the past five years. Single-family residential prices in Snohomish County have increased by 113% over the past decade and by 52% over the past five years. Sellers have made remarkable gains, and success should not be measured by the froth of a seller’s market, but by the gains of a sale in any market. The big-picture approach often leads to a smooth and profitable transition from one house to the next.

Now, back to the tactics of price positioning. Annual prices typically peak in the spring, and after reviewing the latest May 2025 figures, it appears we have hit the peak for the year. This is about 30-45 days earlier than in 2024 and previous years. Additionally, year-over-year prices are flat and slightly down from 2024, so sellers should consider this when choosing their price with their broker. This, along with the increase in selection, means that sellers need to determine the value point at which a buyer is willing to make an offer when they have more choices. They cannot price based on last year’s market, which had different environmental factors.

One thing we can always count on in life is change. The real estate market is no different. In the case of our local real estate market, this change sits on the shoulders of monumental growth. There is always an opportunity within the change, and staying close to the data helps unearth this. I’m encouraged by the balance in the market and look forward to helping my clients navigate their life transitions in the most effective way possible. Research, data, and listening to my client’s goals are the backbone of my approach. If you or someone you know is experiencing significant life changes that a move could help with, please reach out. We can discuss the big picture, apply the data, and chart a custom plan together. It is always my goal to help keep my clients well-informed and empower them to make strong decisions.

Need to Know: Top Takeaways from our Homeowners Insurance Panel

Last week, my office hosted a panel discussion on the hot topic of homeowners insurance. In the wake of several natural disasters, supply chain issues, and inflation on building materials, homeowners insurance is currently experiencing a “hard market”. Non-renewal and cancellation rates are rising, some carriers are leaving certain states, and specific aspects of a home, like wood-shake roofs, are being more scrutinized. This has caused coverage to increase in cost and, in some cases, not be available. We assembled this panel to get this critical real-time information in front of our clients, so they can adequately care for their home(s).

As your trusted real estate advisor who helps you transact when it is time for a move, I also see it as my role to help you protect your asset through education. While I am not an insurance expert, the esteemed panel of insurance professionals we invited to discuss the state of the homeowners insurance market is an example of a trusted advisor in the homeowners insurance field. Below are my top takeaways from the hour-long guided discussion. You can also access the event recording below, which also includes 30 minutes of Q&A from the audience.

What is RCV (Replacement Cost Value), and why is it important?

RCV is the dollar amount established to determine the cost of rebuilding your home to its pre-damage condition. This is different from market value, which includes the land and location premiums. RCV estimates the cost of materials and labor to restore or rebuild your home at today’s prices. This number is critical, and that is why it is important to always let your carrier know when you have made changes or improvements to your home. NOTE: Some carriers use ACV (Actual Cost Value), but this is not preferred as it takes into account depreciation.

Request an annual review of your policy with your carrier.

Most carriers have some built-in annual coverage adjustments, but they are often insufficient. The homeowner is responsible for reporting upgrades, additions, and improvements to their carrier so the increase in investment translates to coverage. Record-keeping of invoices and receipts helps establish accurate replacement value. Notifying your carrier of these changes will capture the appropriate coverage.

Request and review the Declaration Page in your policy.

The declaration page in your policy provides a detailed overview of your coverage. It lists what is covered, the RCV, notes additional riders, and outlines your premiums and deductibles. This is a valuable tool for helping you understand your policy and ensure that everything you have done to your home is included. You can easily request this from your carrier, and it should lead the discussion at your annual review.

Coverage vs. cost matters!

Carriers often advertise and try to appeal to customers based on the affordability of their rates. While no one wants to overpay for insurance, you must analyze the cost-benefit of adequate and complete coverage over the cheapest policy. Oftentimes, the cheapest premiums will lead to your home being underinsured.

Consider adding specific riders for additional coverage.

Unfortunately, earthquake and water backup riders are not included in your basic policy. However, you can purchase these specific riders to add them to your policy and be covered should damage be caused by an earthquake or your sewer line backing up into your home and causing a flood. Adding riders for personal property, such as fine jewelry, is common. These will be listed on your declaration page for an easy accounting of your coverage. Make sure you ask your insurance professional what other rider options are available, so you don’t miss something you would like covered.

Align your deductible with your claim tolerance.

You want to analyze at what point you would make a claim if something happened to your home. The theory of only making a claim if the repair or replacement amount is catastrophic is a good rule of thumb to ensure your policy is not dropped, non-renewed, or wildly increased in premium. What is catastrophic for one person may not be for another, so it is a personal preference around your financial comfort. What you don’t want to have happen is to make a claim on something you could handle on your own, and then have something big happen and no longer be covered. Always consult your insurance professional off-the-record before contacting the carrier directly, so your decision-making is not misconstrued as a claims risk.

Maintain your home to protect your premium.

Due to the industry’s tight margins, many carriers are visiting properties and performing drive-by and/or drone inspections to help determine their risk exposure. They are also accessing Google Earth to make these determinations. Homes that do not appear well-maintained are penalized with premium increases and sometimes dropped by their carriers. This is also why opening and reading all mail from your insurance carrier is essential.

The home and the human are considered in the coverage.

The home’s condition will play into the coverage and premiums, as will the human who is purchasing the policy. Carriers will examine a person’s claims history to help determine their risk exposure. It is common to look back 36 months, and if a person has multiple claims in that timeframe, they will have higher premiums and, in some cases, not be able to purchase coverage.

Have a good relationship with your insurance professional.

Whether working with an insurance broker or a captive company, having a consistent relationship with your provider is valuable. They should be available to answer questions, help you decide whether to make a claim, and review your policy and riders annually. You should never call the carrier directly without first contacting your insurance professional. They can help you navigate important decisions that will keep your coverage intact and your premiums manageable.

I hope you found this information useful—I know I did! It drove home my responsibility of managing my policy and ensuring I am adequately insured through communication with my insurance professional. Much like real estate, having a trusted advisor regarding homeowners insurance is crucial. After all, our home is often our largest asset and most prized possession. Protecting it is critical! Click HERE to access the recording (Passcode: E+gmk9V*) to watch the panel discussion.

As always, please don’t hesitate to reach out if you have any questions or concerns about your property, and I can help guide you to the right answers. I have reputable referrals to multiple insurance professionals that can help you should you need additional contacts. My goal is always to help keep my clients informed and empower them to make strong decisions.